Weekly Market Update by Retirement Lifestyle Advocates

Weekly Market Update by Retirement Lifestyle Advocates

The move away from the US Dollar around the globe continues to accelerate, as confirmed by a brief review of the headlines from the past week.

This is from Michael Maharrey (Source: https://schiffgold.com/key-gold-news/china-brazil-trade-deal-ditches-the-dollar/):

More bad news for the dollar.

Last week, China and Brazil announced a trade deal in their own currencies, completely bypassing the dollar.

This represents another small shift away from dollar dominance.

Under the new deal, Brazil and China will carry out trade directly, exchanging yuan for reais and vice versa instead of first converting to dollars.

In a statement, the Brazilian Trade and Investment Promotion Agency (ApexBrasil) said the agreement would “reduce costs” and ” promote even greater bilateral trade and facilitate investment.”

Brazil ranks as the largest Latin American economy, and China is its biggest trade partner. Trade between China and Brazil amounts to some $150 billion per year. China overtook the US as Brazil’s number-one trading partner in 2009.

China also has dollarless trade agreements with Russia, Pakistan and Saudi Arabia.

This is the latest blow to dollar hegemony. Earlier this year, Saudi Arabia Finance Minister Mohammed Al-Jadaan said the country is open to discussing trade in currencies other than the US dollar. This could mark the beginning of the end of petrodollar exclusivity. And in March, Reuters reported that recent oil deals between India and Russia have been settled in currencies other than dollars.

We are still a long way from the dollar losing its status as the world reserve currency, but its dominance is clearly eroding.

And this from Matthew Piepenberg (Source: https://goldswitzerland.com/golden-question-is-the-petrodollar-the-next-thing-to-break/)

As I’ve presented elsewhere, history (borrowing from Mark Twain) may not repeat itself, but it certainly rhymes.

And toward this end, Rutherglen and Gromen have shown the poetry of rhyming patterns in the context of the ever-changing petrodollar politics, which, modestly, we too foresaw over a year ago.

As we warned from literally day-1 of the western sanctions against Putin, the end result would be disastrous for the West in general and the USD in particular.

And nowhere was this US Dollar prognosis truer than with regard to the petrodollar—i.e., those good ol’ days when nearly every oil purchase was linked to the USD.

However, and as Gromen and Rutherglen suggest, that oil-USD linkage was never a sure thing in the 70’s, and will be even less of a sure thing in the years ahead.

And this, folks, will have a massive impact on gold in the years ahead.

How so?

Let’s dig in.

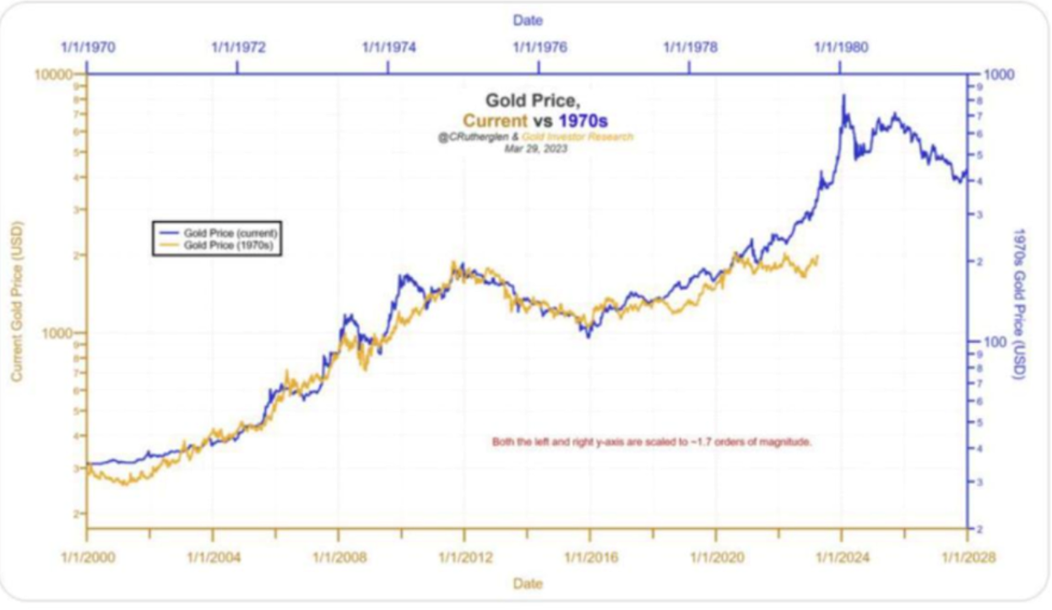

Although still in diapers when Nixon closed the gold window in 71, and still watching Saturday morning cartoons when gold soared from $175/ounce in 1975 to over $800/ounce less than five years later…

… I am at least old enough now to glean a few historical lessons and patterns which may point toward similar and rising gold valuations tomorrow.

Gold, as Gromen and Rutherglen remind, was ripping in the late 70’s largely because it was not yet a foregone conclusion that oil would be pegged to USDs.

In that bygone era of disco, ABBA, wide neckties and checkered suits, neither OPEC nor Europe was against the idea of settling oil transactions in gold rather than USTs.

This was because those very same USTs (thanks to Nixon’s welch) were not very well…loved, trusted or valued in the 70’s.

(See where I’m going [rhyming] with this?)

Fortunately, Paul Volcker was able to seduce the oil nations into trusting Uncle Sam’s fiat money by cranking (and I do mean cranking) interest rates to the moon to restore faith in the UST and hence give OPEC the confidence to sell oil in dollars rather than settle in gold.

Specifically, Volcker took rates to 15+%, a move which placed real rates on that all-important 10Y UST at +8%.

Such hawkish policy was thus a game changer for making the petrodollar a reality and hence the USD the world’s reserve energy asset (and bully) for a generation to come.

Unfortunately, and thanks to Uncle Sam’s embarrassing bar tab (i.e., debt levels), those days, and those USDs and USTs, have fallen from grace and hence are slowly falling off the radar of OPEC.

For this, we can also thank an openly cornered Powell’s so-called war on inflation, which has, among so many other backfired fiascos, led to a slow and steady process of de-dollarization and declining faith in that oh-so-important global IOU, otherwise known as the UST.

The Oil Nations Aren’t Stupid

The OPEC folks know that Uncle Sam’s IOU’s aren’t what they used to be.

Unlike Volcker, however, Powell can’t get the 10Y UST to an 8% real (i.e., inflation-adjusted) rate.

Even his so-called “hawkish” nominal rates of 5% have crushed credit markets, Treasuries and nearly everything else in its path.

And if Powell even dreamed of pushing rates to 15% ala Volcker to seduce OPEC, he would literally murder the entire US economy with a double-digit rate hike against a $31T public debt pile.

In short, there is simply no way to compare Volcker’s options in the 70’s to Powell’s debt reality in 2023.

This means the Fed can’t do what will be needed this time around to prevent OPEC from looking outside the USD or UST and hence inside the gold markets as a primary asset to settle its energy transactions.

The days of the mighty petrodollar, as I warned (in two languages) over year ago here, here and here, are slowly but steadily coming to end.

Think about that for a second.

Or better yet, look at it for a second—with kudos again to Gromen and Rutherglen.

Piepenberg makes the same argument that I have been making – the Fed will HAVE to pivot. It’s either that or destroy the economy. I make this statement understanding that there are some very bright analysts who disagree.

But, the emerging economic and geo-political conditions indicate that there can be no other outcome in my view.

The radio program this week features an interview with Mr. Karl Deninger.

Karl and I discuss the current state of the banking system, the new currency talk from BRICS, and the future of central bank-issued digital currencies. You can listen to the show now by clicking on the "Podcast" tab at the top of this page.

“It is the mark of an educated mind to be able to entertain a thought without accepting it.”

-Aristotle

Comments