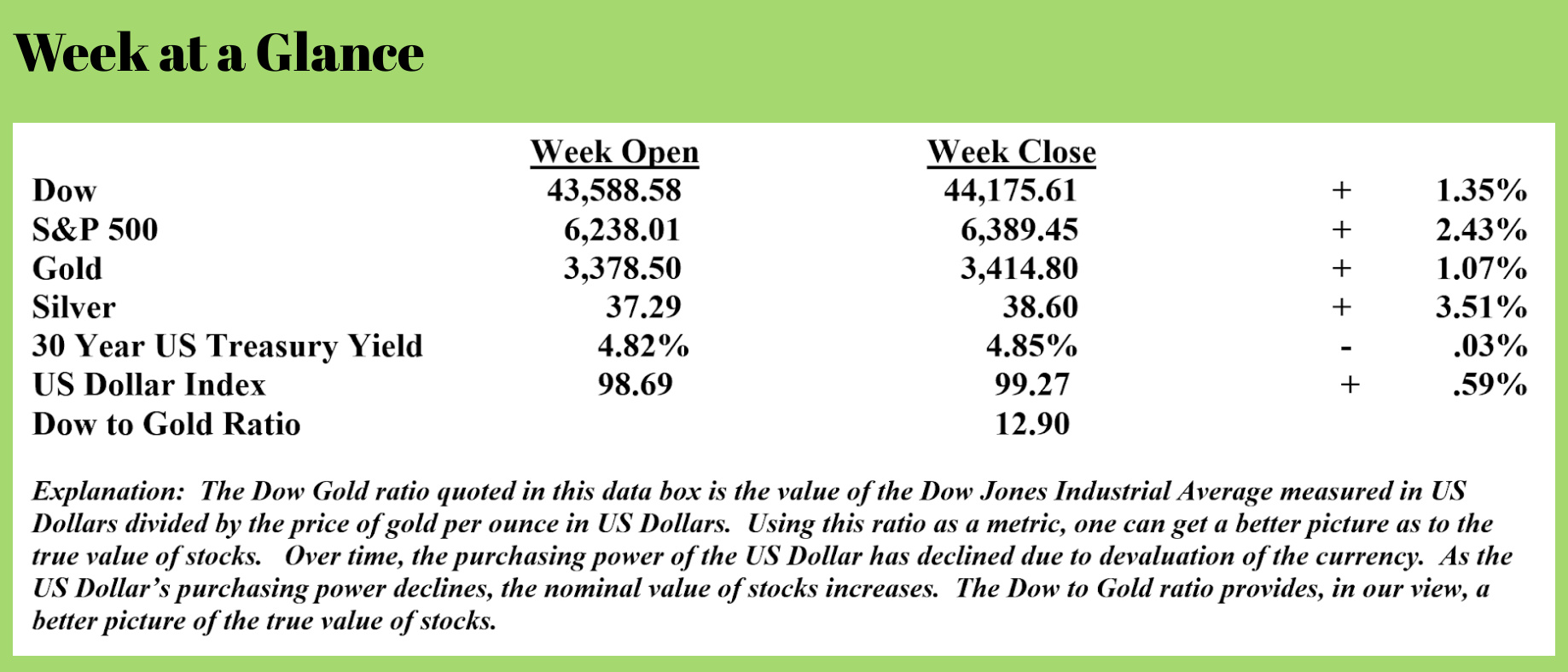

Weekly Update from RLA Tax and Wealth Advisory

Weekly Update from RLA Tax and Wealth Advisory

Future Inflation Assured

A report from the US Treasury Department that got very little media attention (no surprise there) revealed that the US Government has official debt of more than $37 trillion but total obligations of more than $151 trillion. (Source: https://starkrealities.substack.com/p/america-37-trillion-national-debt-far-worse-unfunded-liabilities)

A law passed in 1994 requires this report from the Treasury to convey, annually, the total of unfunded liabilities of the U.S. Government. Unfunded liabilities are spending commitments made by the government that have no earmarked assets or income sources from which to pay the obligations.

If you’re wondering why the discrepancy is so large, that is a fair question. The simple answer is the accounting system that the government uses. Rather than using an accrual accounting system that records expenses when they are incurred, the government uses a cash accounting system that records expenses when they are paid.

In other words, the government uses an accounting system that does not accurately reflect the true state of the government’s finances.

According to the report, the total unfunded liabilities of Social Security and Medicare are $105.8 trillion. On top of that eye-popping number is the unfunded liabilities of federal employee and veteran programs aggregating to $15 trillion.

Officially, the US Government has assets of $7.9 trillion comprised of property, equipment, and official gold holdings. That’s a total government net worth of a negative $143 trillion.

So why does this assure future inflation?

The answer is simply math.

There are only three possible ways to deal with this problem. One is to raise taxes. Scratch this as an option. According to the Federal Reserve, this is 85% of the total net worth of ALL American households. And, to make matters worse, the national debt is increasing at a rate of $156 million per hour!

The second option is to cut spending to balance the budget and then devise a plan to reduce the unfunded liabilities. Reducing the unfunded liabilities of the US Government would require massive cuts to Social Security and Medicare. Not going to happen. Recently, the vice-president had to cast a tie-breaking vote to get $9 billion in spending cuts done, which is just a half percent of the total annual operating deficit.

Which leaves the third option – more, easy money and currency creation. The more severe the debt and underfunding problems become, the more this becomes the only option, which will lead to more inflation.

We are past the point of no return and are no longer debating the ‘what’, only the ‘when’. Is your portfolio allocated to protect you from the inevitable?

More Evidence the Low and Middle-Income Consumer is Struggling

McDonald’s corporation did recently beat earnings estimates, but company leadership is openly stating that inflation and the current economy are really hurting the low-income consumer. (Source: https://www.zerohedge.com/personal-finance/mcdonalds-execs-reveal-working-poor-customers-skipping-breakfast)

Specifically, McDonald’s reported that breakfast was the restaurant chain’s worst-performing meal. McDonald’s CFO, Ian Borden, stated, “With the low-income consumer, despite improvements in wage gains, real incomes are down. So, real incomes are down with the low-income consumer. That absolutely is going to put pressure on visits into the QSR industry.”

Borden added that low-income consumers are ‘skipping a daypart like breakfast, or they’re trading down either within our menu, or they’re trading down to eating at home.”

While inflation continues to erode the spending power of the dollar, particularly among low-income consumers, this could be a leading indicator for the consumer spending-dependent US economy.

Loan Delinquency Rates Continue to Climb

According to the New York Federal Reserve, delinquency rates at the end of June on all outstanding debt was 4.4%. That’s up .1% from the first quarter. (Source: https://www.newyorkfed.org/medialibrary/interactives/householdcredit/data/pdf/HHDC_2025Q2)

Student loan debt, in particular, stood out in the report. Total student loan debt stood at $1.74 trillion. The percentage of outstanding student loan debt that was more than 90 days delinquent was 10.2%.

Credit card delinquency rates rose to 12% and auto loan debt to 5%. All these percentage delinquent rates are higher than the prior month.

Alarmingly, debt accumulation by consumers is continuing to rise. Total household debt rose by $185 billion in the second quarter of this year. (Source: https://wolfstreet.com/2025/08/05/household-debts-debt-to-income-ratio-serious-delinquencies-collections-foreclosures-bankruptcies-our-drunken-sailors-debts-in-q2-2025/)

Year-over-year, household debt grew by $592 billion.

Mortgage balances grew by $131 billion during the second quarter, and Home Equity Lines of Credit saw balances increase by $9 billion. (Source: https://www.zerohedge.com/markets/shocking-record-explosion-student-loan-delinquencies-marks-start-next-debt-crisis)

Credit card balances, despite rising delinquencies, rose by $27 billion during the second quarter. Credit card debt is now 5.87% higher than one year ago.

Auto loan balances rose by $13 billion during the second quarter, and student loan debt increased by $7 billion.

Rising delinquency rates on existing debt, along with rising debt levels, are a one-two punch that may eventually result in a recession.

Couple that with overvalued stock and real estate values, and there may be a perfect setup for declining asset values, at least in real terms.

RLA Radio

The RLA radio program this week features an interview that I conducted with Dr. Robert McHugh, a very bright technical analyst. I get Bob’s forecast for multiple markets based on his analysis. The interview is available now by clicking on the "Podcast" tab at the top of this page.

Quote of the Week

“Where facts are few, experts are many.”

-Donald R. Gannon

Comments