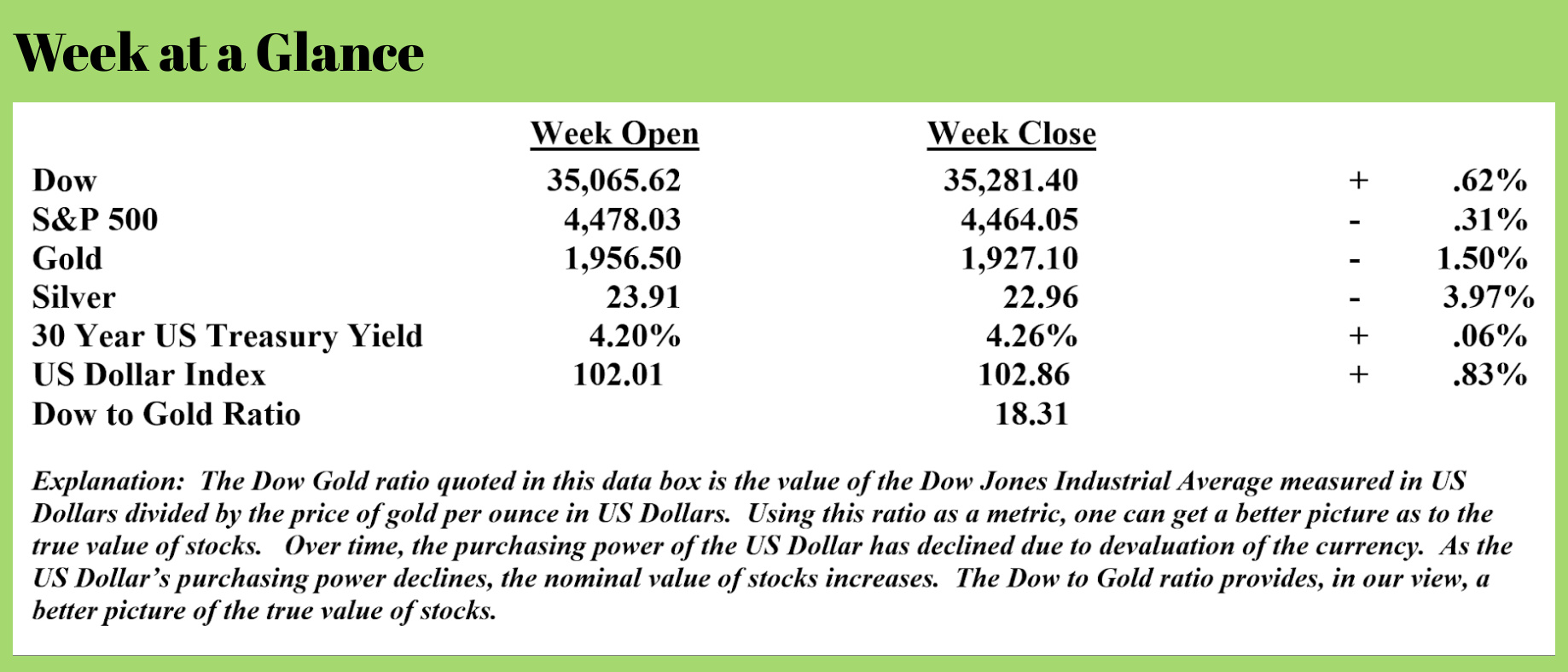

Weekly Market Update by Retirement Lifestyle Advocates

Weekly Market Update by Retirement Lifestyle Advocates

I’ve been making the case that the US consumer is stretched to the point that the economy is being affected, soon, very noticeably affected.

The US economy is more than 70% dependent on consumer spending, and when the consumer can’t spend, the economy suffers. It really is that simple.

Despite the fact that Federal Reserve Chairman Jerome Powell recently made comments that the Fed is no longer forecasting a recession but rather a ‘noticeable slowdown’ (whatever that means exactly), the data seems to suggest that consumers are suffering, and a recession may be looming.

Author Michael Snyder recently commented on this very topic, citing 9 data points that indicate the US consumer may be at his or her breaking point. (Source: https://endoftheamericandream.com/9-signs-that-the-u-s-consumer-is-about-to-break/).

Reason number one offered by Snyder is that after adjusting for inflation and taxes, the income of US consumers has fallen by more than 9% since April of 2020. That’s noteworthy, to say the least.

This, from Snyder’s piece:

On the inflation issue, household income adjusted for inflation and taxes is running some 9.1% below where it was in April 2020, putting additional pressure on consumers, according to SMB Nikko Securities.

Snyder then makes a point that I’ve been making repeatedly – consumers are turning to credit cards to a greater extent than ever to help make ends meet. On this week’s Headline Roundup webinar (replay available at www.RetirementLifestyleAdvocates.com), I noted the recent MSNBC article that reported credit card debt has now exceeded the $1 trillion threshold for the very first time in history.

Here is a bit from the article (Source: https://www.cnbc.com/2023/08/08/credit-card-balances-jumped-in-the-second-quarter-and-are-above-1-trillion-for-the-first-time.html):

Americans increasingly turned to their credit cards to make ends meet heading into the summer, sending aggregate balances over $1 trillion for the first time ever, the New York Federal Reserve reported Tuesday.

Total credit card indebtedness rose by $45 billion in the April-through-June period, an increase of more than 4%. That took the total amount owed to $1.03 trillion, the highest gross value in Fed data going back to 2003.

The increase in the category was the most notable area as total household debt edged higher by about $16 billion to $17.06 trillion, also a fresh record.

“Household budgets have benefitted from excess savings and pandemic-related debt forbearances over the past three years, but the remnants of those benefits are coming to an end,” said Elizabeth Renter, data analyst at personal finance site NerdWallet. “Credit card delinquencies continue an upward trend, a growing sign that consumers are feeling the pinch of high prices and lower savings balances than they had just a few years ago.”

As card use grew, so did the delinquency rate.

The Fed’s measure of credit card debt 30 or more days late climbed to 7.2% in the second quarter, up from 6.5% in Q1 and the highest rate since the first quarter of 2012 though close to the long-run normal, central bank officials said. Total debt delinquency edged higher to 3.18% from 3%.

Snyder also points out that the delinquency rate on credit cards is rising as interest rates have increased. The average interest rate on credit card balances is now more than 20%, according to Bankrate and as cited in the article by Snyder.

Snyder also points out another bit of data, the meaning of which cannot be denied. Emergency withdrawals from retirement accounts are rising. By more than 35% year-over-year. This, once again from Snyder’s piece:

More Americans are tapping their 401(k) accounts because of financial distress, according to Bank of America data released Tuesday.

The number of people who made a hardship withdrawal during the second quarter surged from the first three months of the year to 15,950, an increase of 36% from the second quarter of 2022, according to Bank of America’s analysis of clients’ employee benefits programs, which are comprised of more than 4 million plan participants.

As withdrawals from retirement accounts surge along with credit card balances, many Americans have been priced out of the housing market due to rapidly increasing interest rates. This, again from Snyder:

Elevated mortgage rates and sales prices mean owning a home is about 20% more expensive than it was last year.

The typical U.S. homebuyer’s monthly mortgage payment was $2,605 during the four weeks ending July 30, down $32 from July’s record high but up 19% from a year prior, according to a Friday report from real estate listing company Redfin.

Rents are also increasing rapidly meaning consumers have no refuge from rapidly increasing housing costs.

Snyder points out that for the past two years, the average rent-to-income ratio has exceeded 30%. This means that the AVERAGE rent that a person pays is more than 30% of their income. This from “Fox Business” (Source: https://www.foxbusiness.com/economy/us-renters-remain-burdened-some-metro-areas-saw-relief-first-half-year):

The nationwide average rent-to-income ratio declined slightly in the first half of this year, declining to 30.2% from a high of 30.8% last year – which was the first time ever that median-income renter households paid more than 30% of their income on an average-priced apartment. Renters are considered "burdened" if their rent consumes 30% or more of their gross, or pre-tax, income.

"What that means is, by and large, the U.S. is still rent burdened because we are officially above that 30% rent-burdened threshold," Lu Chen, a senior economist at Moody’s Analytics specializing in commercial real estate, told FOX Business. "We are seeing levels of relief but also combined with the inflationary pressure elsewhere, so we're still spending a little higher on the necessities – on food and energy along with other necessary spending."

Snyder notes that the cost of vehicle repairs is also up meaningfully. This from his piece:

Car repair costs are up almost 20% in the past year, according to the consumer price index — more than six times the national inflation rate and among the largest annual price increases of any household good or service.

So, what’s driving up prices?

It’s a combination of factors, experts said. Some emerged in the pandemic era, while others are longer-term trends in the auto market, they said.

Finally, perhaps the most sobering statistic of all. Nearly 70% - yes, 70% - of urban American consumers are now living paycheck-to-paycheck.

This from “PR Newswire” (Source: https://www.prnewswire.com/news-releases/69-of-americans-in-urban-areas-are-living-paycheck-to-paycheck-14-percentage-points-higher-than-suburban-consumers-301832741.html)

LendingClub Corporation (NYSE: LC), the parent company of LendingClub Bank, America's leading digital marketplace bank, today released findings from the 22nd edition of the New Reality Check: The Paycheck-to-Paycheck research series, conducted in partnership with PYMNTS. The Regional Divide Edition examines why U.S. consumers in urban, suburban and rural areas across the U.S. are living paycheck to paycheck and identifies the financial stressors they face. This edition is based on a census-balanced survey of 3,652 U.S. consumers conducted from April 3 to April 17 as well as analysis of other economic data.

Key takeaway: Consumers are facing financial challenges based on their location that lead them to live paycheck to paycheck, with urban dwellers and those earning the highest salaries more apt to feel the pain of inflationary pressures and the rising cost of living.

Sixty-one percent of consumers overall were living paycheck to paycheck in April 2023, a level similar to April 2022. In fact, since March 2020, an average of 60% of consumers have reported living this way. For those Americans, this means that they need their next paycheck to cover their monthly financial outflows.

The share of high-income consumers in the U.S. earning over $100,000 per year who live paycheck to paycheck increased seven percentage points to 49% in April 2023 from 42% in April 2022. Conversely, the share of lower-income consumers — those earning less than $50,000 — who live paycheck to paycheck dropped seven percentage points from 80% to 73% in the same period, and the portion of those earning between $50,000 and $100,000 remained roughly flat at 63%.

The radio program this week features a ‘best-of’ interview with Mr. Michael Oliver, founder and President of MSA, Momentum Structural Analysis.

Michael was ahead of the curve in adjusting his analysis to account for fiat currency devaluation, and his work is excellent.

I know you’ll enjoy my conversation with him. If you haven't yet listened, click on the "Podcat" tab at the top of this page to listen now!

“If you try to fail and succeed, which have you done?”

-George Carlin

Comments