Weekly Market Update by Retirement Lifestyle Advocates

Weekly Market Update by Retirement Lifestyle Advocates

Is this the “Everything Bubble”?

Past radio program guest, Mr. John Rubino, made a great case that we are now experiencing a bubble, unlike any bubble we’ve experienced historically.

I have long been stating the same thing, pointing at stocks, bonds, and real estate in particular.

Rubino, in his recent article (Source: https://www.dollarcollapse.com/biggest-financial-bubble-hell-yes/) points out that if someone today is over age 40, they have lived through at least three bubbles: there was the junk bond bubble of the 1980’s, the tech stock bubble of the 1990’s and the housing bubble of the 2000’s.

Each of these bubbles occurred as a result of easy money policies, but, as Mr. Rubino points out, they affected only a single sector of the financial markets.

This bubble looks different and it looks like it’s affecting almost every financial sector.

Bubbles use easy money as their fuel. Without easy money, bubbles cannot form. Easy money, as we’ve discussed in past issues of “Portfolio Watch” is easy credit. Today, easy money combines easy credit and money creation literally out of thin air.

This combination makes the bubbles even bigger.

Taking a look at money creation over the past 20 years since the turn of the century, one finds that the US money supply has more than tripled with money creation last year alone increasing by more than 1/3rd.

That’s a lot of easy money to get bubbles going in a lot of different areas.

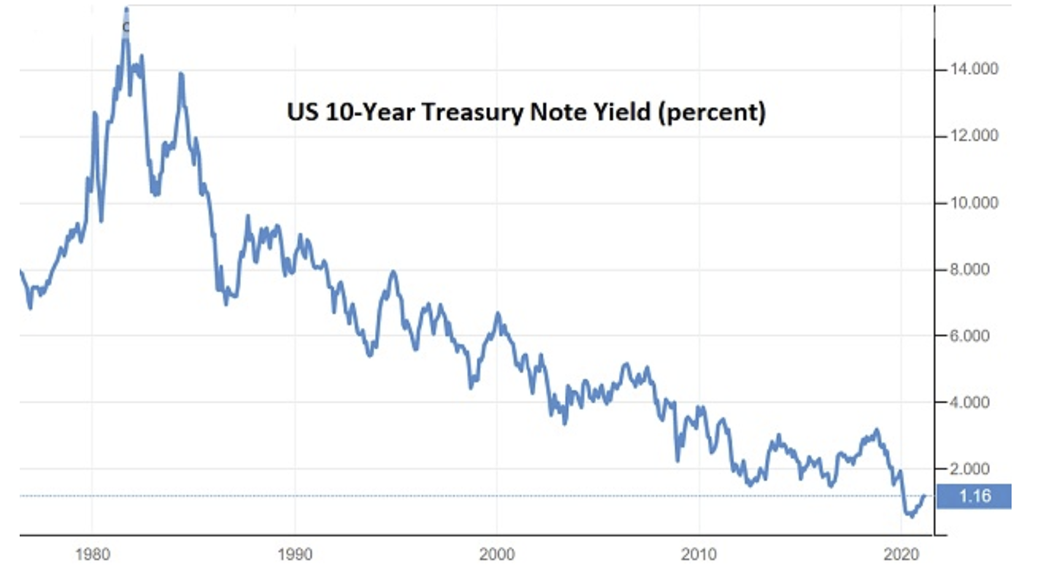

While bond yields have started to rise meaning bonds are losing value (bond yields and prices are inversely correlated, when bond yields rise, it means bond prices are falling), over the longer time frame, yields have fallen dramatically which means price have risen significantly. The chart illustrates the yield of the 10-Year US Treasury Note. Since 1980, yields have been declining which means prices have been rising.

While bond yields have started to rise meaning bonds are losing value (bond yields and prices are inversely correlated, when bond yields rise, it means bond prices are falling), over the longer time frame, yields have fallen dramatically which means price have risen significantly. The chart illustrates the yield of the 10-Year US Treasury Note. Since 1980, yields have been declining which means prices have been rising.

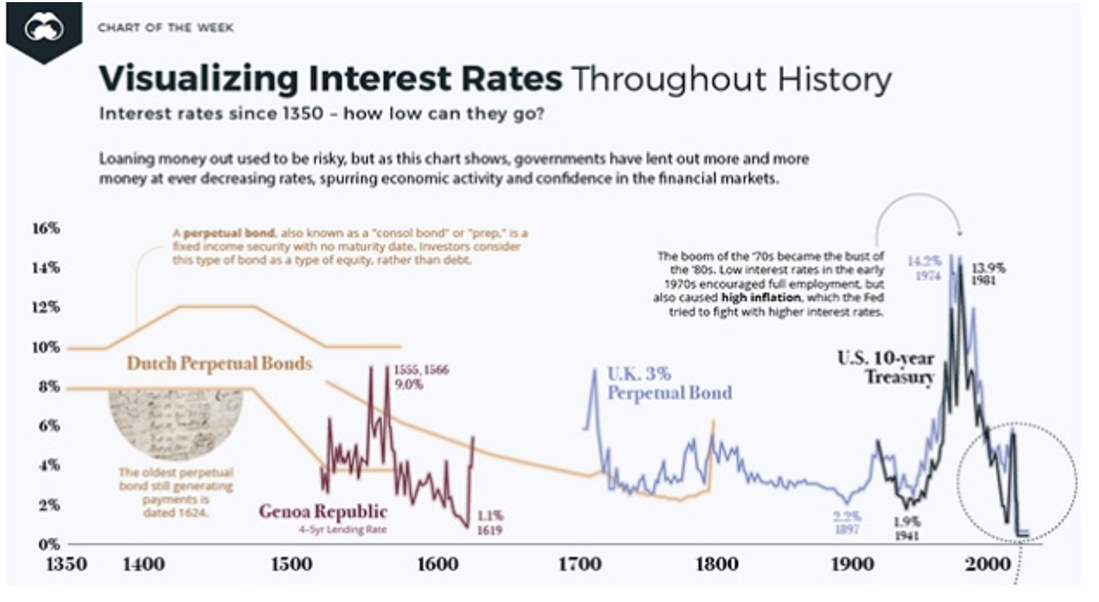

Lest you think this is normal behavior for bonds, John Rubino published this chart that clearly demonstrates today’s bond yields are the lowest in human history. The chart, titled “Visualizing Interest Rates Throughout History” shows that going back to 1350, interest rates have never been this low. That means bond valuations have never been this high and we all know these nosebleed bond valuation levels are not because the credit risk of the bond issuers is low. Quite the contrary, interest rates are artificially low while credit risk is rising. It’s a perfect storm for a bond bubble.

Lest you think this is normal behavior for bonds, John Rubino published this chart that clearly demonstrates today’s bond yields are the lowest in human history. The chart, titled “Visualizing Interest Rates Throughout History” shows that going back to 1350, interest rates have never been this low. That means bond valuations have never been this high and we all know these nosebleed bond valuation levels are not because the credit risk of the bond issuers is low. Quite the contrary, interest rates are artificially low while credit risk is rising. It’s a perfect storm for a bond bubble.

But, it’s not just bonds that are in a bubble; for a long while now, I’ve been warning that stocks are overvalued. While my technical stock indicators have stocks in a solid uptrend, they are overbought and stock fundamentals don’t support these valuation levels.

But, it’s not just bonds that are in a bubble; for a long while now, I’ve been warning that stocks are overvalued. While my technical stock indicators have stocks in a solid uptrend, they are overbought and stock fundamentals don’t support these valuation levels.

Using the “Buffet Indicator” to measure the value of stocks, as seen on the chart, stocks are more overvalued presently than at any time in the last 30 years.

Stocks, using the Buffet Indicator are more overvalued presently than at the peak of the tech stock bubble two decades ago.

While the last big bubble was in housing a little more than a decade ago, it seems that we are headed in that direction again.

While the last big bubble was in housing a little more than a decade ago, it seems that we are headed in that direction again.

The chart, from the Federal Reserve Bank of St. Louis, shows that housing prices last year went nearly vertical on the chart – a historic sure-fire indicator of a bubble.

While bubbles can build for a longer period of time than one might think, eventually, bubbles have to burst.

It’s easy to argue that there is also a bubble in crypto-currencies.

The chart illustrates Bitcoin price history.

Notice the straight up chart pattern of the chart, a pattern that I would call parabolic. Regardless as to what you call the pattern, straight up on charts are almost always followed by straight down in my experience.

Notice the straight up chart pattern of the chart, a pattern that I would call parabolic. Regardless as to what you call the pattern, straight up on charts are almost always followed by straight down in my experience.

Ethereum, another popular cryptocurrency has a chart price pattern that is even more extreme.

Almost every market and economic sector are now ‘bubbling’ due to all the easy money created by the central bankers at the Federal Reserve.

It seems that the central bankers have no intention of changing course any time soon.

Fed Chair, Jerome Powell, is committed to even more easy money policies moving ahead.

Reading between the lines, it’s obvious that the Fed understands the risks of much higher inflation that will likely accompany these continued policies.

Last year, the Fed changed the way the central bank would track the inflation rate. The new inflation tracking methodology is Average Inflation Targeting. This allows the Fed to let inflation run hotter than the desired level for a period of time as long as the average rate is at the Fed’s targeted rate.

No matter the metric used to track the inflation rate, the actual inflation rate seems certain to rise.

While last year’s federal budget operating deficit of a little more than $3 trillion seemed like it could be the straw that broke the proverbial camel’s back, this year’s deficit will make that one look like child’s play.

Prior to the proposed $1.9 trillion stimulus package, this year’s deficit is projected to be $2.3 trillion (Source: https://www.cnbc.com/2021/02/11/deficit-projected-at-2point3-trillion-for-2021-not-counting-additional-stimulus-cbo-says.html). Add the stimulus package in and we could see a deficit of more than $4 trillion with declining GDP.

There is one bubble I did not discuss – a currency bubble.

Seems that the bubble is bursting in painful slow motion as we watch.

If you’d like to get more information on owning hard assets, give the office a call and we can schedule a time to get you more information and educate you on the different ways to own hard assets,

Thank you all for your continued support and referrals. If you know of someone who could benefit from our educational materials, please have them visit our website at www.RetirementLifestyleAdvocates.com. Our webinars, podcasts, and newsletters can be found there.

The radio program this week features an interview with prolific author, Jeffrey Tucker. Jeffrey is an entertaining guy to chat with and an unapologetic libertarian and Austrian economist.

If you are not participating in our weekly Monday update webinars, you can get more information on them at www.RetirementLifestyleAdvocates.com or catch the replays there.

As noted above, if you need more information about the webinars or would like to schedule a phone conversation to discuss precious metals, just give the office a call at 1-866-921-3613.

“Some people see the glass as half full, others see it as half empty. I see a glass that is twice as big as it needs to be.”

-George Carlin