Weekly Update from RLA Tax and Wealth Advisory

Weekly Update from RLA Tax and Wealth Advisory

By: Dennis Tubbergen

Existing Home Sales Slide

According to the National Association of Realtors, home sales fell on a month-over-month basis and on a year-over-year basis. (Source: https://www.nar.realtor/research-and-statistics/housing-statistics/existing-home-sales)

The Chief Economist at the National Association of Realtors, Dr. Lawrence Yun, commented, “The decrease in sales is disappointing. The below-normal temperatures and above-normal precipitation this January make it harder than usual to assess the underlying driver of the decrease and determine if this month’s numbers are an aberration.”

Interesting that Dr. Yun is blaming the weather for lower closed sales in January.

While it’s impossible to argue with the fact that the month of January saw downright miserable weather conditions in much of the United States, it’s also an undeniable fact that home sales that closed in January had purchase contracts that were signed in November or December at the latest, when the weather was not so poor.

The reality is that the difficult weather conditions in January, if they were a contribution factor to lower real estate sales, would not reflect in the sales statistics until February or, more likely, March.

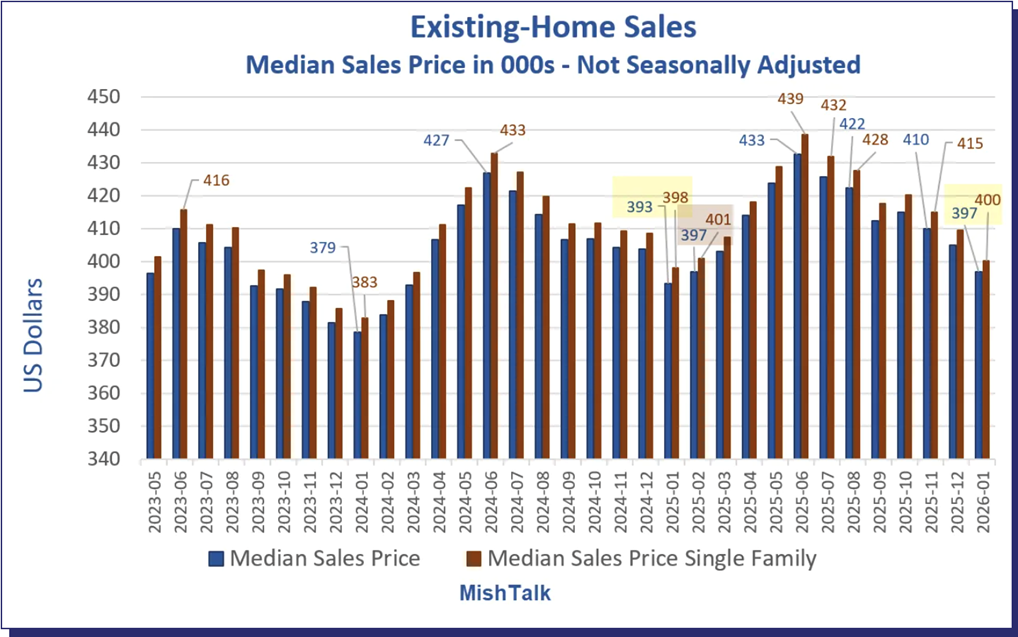

Median sales prices of single-family homes peaked in July of 2025 and have now fallen every month since then, as seen from this chart (Source: https://mishtalk.com/economics/existing-home-sales-plunge-the-most-since-november-2022-the-weather/):

A lower number of closed sales and fallen sales prices are reflective of a weakening market, as I’ve been forecasting here for more than a year.

It’s my view that there is more downside in housing ahead.

Is this a Looming Storm in the Silver Market?

Silver has been one of my favorite speculative investment assets for a couple of years now. And, despite recent price action, it is still one of the assets that I expect will outperform moving ahead.

Not only is industrial demand greater than mining output, but the number of silver (and gold) traders on the COMEX exchange who are standing for delivery is also increasing.

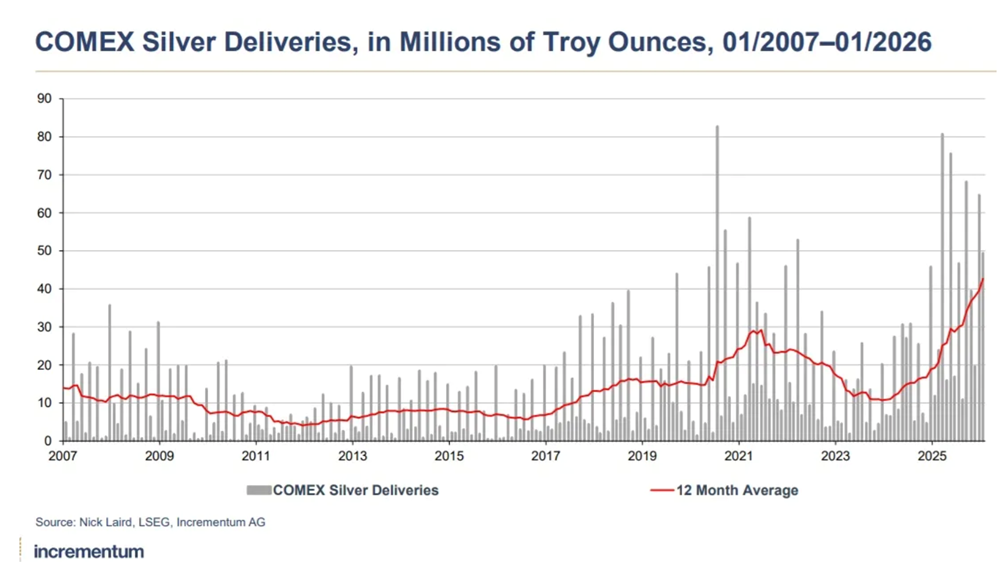

Past RLA Radio Guest, John Rubino, published this chart in his popular Substack newsletter last week (Source: https://rubino.substack.com/p/the-goldsilver-bull-market-in-eight)

The chart illustrates silver deliveries on the COMEX, in millions of ounces, month-to-month, going back to calendar year 2007. The red line on the chart is the 12-month average of monthly deliveries.

The chart illustrates silver deliveries on the COMEX, in millions of ounces, month-to-month, going back to calendar year 2007. The red line on the chart is the 12-month average of monthly deliveries.

Note that the deliveries of physical silver have increased by more than 400% since 2024, about two years ago. That’s telling.

Silver traders are preferring the physical metals to US Dollars. The possible looming storm is that, should this trend continue, supplies of physical silver could run short, and silver prices could move higher.

China Continues to Stack Gold

Gold reserves now officially account for 9% of all central bank reserves.

China has been buying gold and selling US Treasuries. Chinese gold reserves continue to rise month-to-month,h and holdings of US Treasuries are down 10% from just one year ago. (Source: https://www.theepochtimes.com/business/chinas-central-bank-keeps-buying-gold-and-dumping-us-debt-5983835?utm_source=partner&utm_campaign=ZeroHedge)

The trend continues.

RLA Radio

The RLA radio program this week features an interview that I conducted with Brien Lundin, editor of “Gold Newsletter” and the host of the largest investment conference in the world.

Brien and I discuss the current state of the precious metals market and the world economic outlook, and how aspiring retirees might be affected. The podcast is available by clicking on the "Podcast" tab at the top of this page.

Quote

“Although golf was originally restricted to wealthy, overweight protestants, today it is open to anybody who owns hideous clothing.”

-Dave Barry

Comments