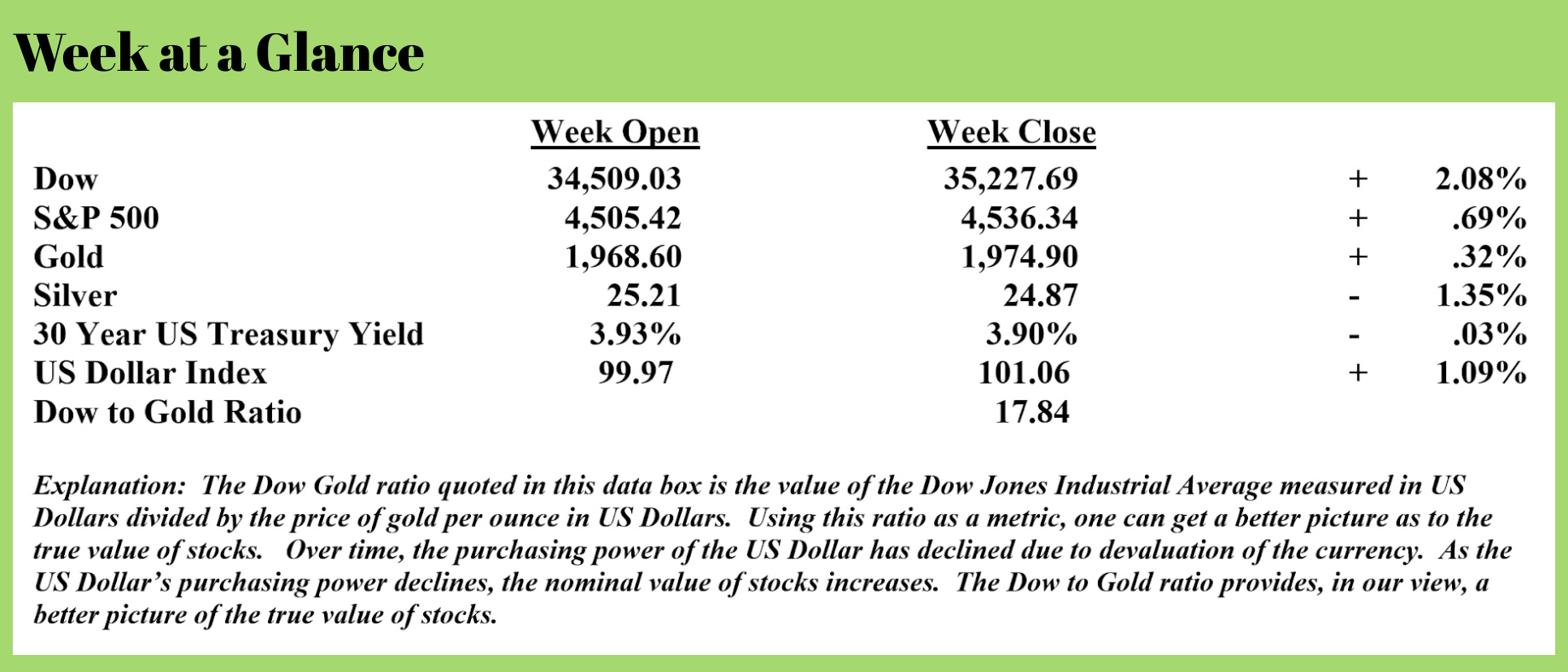

Weekly Market Update by Retirement Lifestyle Advocates

Weekly Market Update by Retirement Lifestyle Advocates

In my 2011 book “Economic Consequences,” I examined the notion of unintended consequences. I offered several examples of government actions that may have been taken with good intentions (we can debate that another time), but ended up causing unpleasant, unintended consequences.

A couple of examples are the Americans with Disabilities Act and the Endangered Species Act. The Americans with Disabilities Act has actually resulted in fewer disabled people working, and the Endangered Species Act, designed to preserve the natural habitat of species that the government considers to be endangered, has actually resulted in habitat being destroyed.

This is a common result of bureaucratic action. Seems that Americans collectively don’t like being told what to do. Owners of land that could be considered the habitat of an endangered bird or animal at some future point log the land or change the character of the land before such a declaration can be made.

The City of Detroit (and other major US Cities) began their descent into their current, dilapidated state as a result of the Model Cities program of the 1960’s.

Now, it seems, the real estate market is beginning to suffer as a result of the Fed’s extremely low, totally artificial interest rate policy over the past several years.

While interest rates were artificially low, and a 30-year mortgage could be had for a 3% fixed interest rate (or even lower), many homeowners bought a new home or refinanced an existing home.

Now, many of those homeowners are financially unable to make another move due to interest rates returning to a more ‘normal’ level.

Wolf Richter commented (Source: https://wolfstreet.com/2023/07/21/entire-housing-market-buyers-and-sellers-may-have-shrunk-by-20-25-because-of-the-3-mortgages/)

The exact numbers are hard to nail down, but we can guesstimate from the figures we have that the entire housing market, both buyers and sellers, has shrunk this year by about 20% to 25% compared to pre-pandemic years.

Meaning 20% to 25% less demand and sales and 20% to 25% less inventory and new listings, with prices down a tad year-over-year, showing that the market is roughly balanced at this smaller size because buyers and sellers have vanished in equal numbers.

And we know who they are: the homeowners in 3%-mortgage jail that now cannot buy and, therefore, cannot sell.

The 3% mortgages that a lot of homeowners now have after the huge refinancing boom during the pandemic prevent those people from buying a new home because they might have to finance it at about 7%, which would increase the monthly payment on the same size mortgage by 50% or more.

To put some numbers to Mr. Richter’s statement, a 30-year mortgage in the amount of $350,000 at 3% interest results in a payment of $1,476 monthly. When the interest rate on the same 30-year mortgage rises to 7.25%, the payment increases to $2,388 per month!

That’s an increase of about 62%!

While real estate agents loved the 3% mortgage at the time it existed, considering it to be a gift, they are now viewing it as a curse. More from Mr. Richter’s piece:

These homeowners with 3% mortgages don’t want to, or cannot, upsize or downsize, or move to a different location, move closer to the kids or parents, or whatever – unless they want to give up their sacred 3% mortgage that now increasingly looks like a gift from God.

And for Realtors, the 3% mortgage – as much as they loved it at the time – has now turned into a gift from hell, because the real estate industry is making commissions coming and going: One, when these homeowners sell their old home, and two, when they buy a new home.

Each household that is now prevented from changing homes because they’re locked in by this 3% gift from God subtracts two transactions from the market – one when they buy a new home, and the other when they sell their old home. And Realtors are losing both of those deals.

The fact that Realtors are losing both of those deals is why the industry is so upset about these homeowners that refuse to sell – and it consistently blames them for the low inventory.

But the industry fails to state the other half of this reality, though they all know it: That these homeowners who refuse to sell have also vanished as buyers, and therefore this portion of demand has dropped in equal measure with inventories.

This is happening with a fairly large group of homeowners: They have left the market as both sellers and buyers at the same time and in equal numbers.

Which explains in part why sales volume has plunged so far because those potential buyers with 3% mortgages have left the market. And it explains in part why inventories have dropped because the same people that cannot buy aren’t putting their homes on the market.

Seems that the Fed’s artificially low-interest rate environment is now resulting in the emergence of some unintended consequences. Mark my words; there will be additional, more harsh economic consequences emerging soon.

Artificially low-interest rates result in debt accumulation. Ironically, the Fed’s response to the financial crisis, caused by debt excesses, was to promulgate a monetary policy that resulted in even more debt accumulation.

Keep in mind that in a fiat currency system, all money is debt. This means that when debt goes unpaid or is defaulted upon, the money/currency supply contracts resulting in recession or depression (depending on the debt levels that exist).

While I believe that we are currently in a recession, I am also of the mind that the current economy will continue to deteriorate.

Let me share just one statistic with you that makes me believe that the economy has tough days ahead and that the Fed’s artificially low-interest-rate environment will ultimately lead to even more severe, unintended economic consequences.

This from the “Motley Fool” (Source: https://www.fool.com/investing/2023/07/02/money-supply-since-great-depression-big-move-stock/):

Though there are a few variations of money supply, most economists tend ot focus on M1 and M2. The former takes into account cash and coins in circulation, as well as demand deposits in checking accounts and traveler’s checks. In other words, money that is either in your hand or can be accessed very easily.

Meanwhile, M2 accounts for everything in M1 and adds savings accounts, money market funds, and certificates of deposit (CD’s) below $100,000. It’s money you have access to, but it takes a little extra effort to put this capital to work. It’s M2 money supply that’s raising eyebrows on Wall Street and making history.

During the COVID-19 pandemic, M2 soared 26% on a year-over-year basis, which represents the steepest increase in US money supply when back-tested to 1870. The issuance of multiple rounds of stimulus checks to the American public, along with pandemic-based programs for businesses, pumped capital into the US economy at an extraordinary pace. Unsurprisingly, historically high inflation – 9.1% at the peak in June 2022 –soon followed.

What’s of interest is what’s happened to M2 money supply over the trailing year. Following a peak of $21.7 trilion in July 2022, M@ has fallen to a fresh reading of $20.81 trillion as of May 2023. Although the May reading was higher than April and broke a nine-month downtrend, we’ve still witnesses a 4.1% aggregate drop in M2 from it’s all-time high.

Considering that M2 enjoyed a historic expansion during the pandemic, it’s certainly possible that a 4.1% decline can be shrugged off as nothing more than money supply reverting back to the mean. But history suggests otherwise.

Though history rarely repeats itself on Wall Street, it often rhymes. We haven’t seen a meaningful year-over-year decline in M2 money supply since the Great Depression in 1933.

I have long forecasted that we would see inflation followed by deflation. The contraction of the money supply may be the first warning that deflation is emerging.

In the meantime, despite the tough talk from the Fed, I fully expect that the central bank will eventually pivot, reverting to easy money policies.

It remains to be seen if the Fed can be successful in staving off deflation – I have my doubts.

The most likely outcome near-term, in my view, is stagflation – rising consumer prices combined with a contracting economy.

That economic climate will then likely morph into full-blown deflation, taking down stocks and real estate.

If you are not using the Revenue Sourcing planning process in your personal financial situation, it may be time to take a closer look.

The radio program this week features an interview with the Head of Global Research at Elliott Wave International, Mr. Murray Gunn.

I get Murray’s forecast for stock markets and bond markets, as well as the world economy.

We also chat about a very interesting science developed by Elliott Wave – Socionomics, which makes economic and investing forecasts based on social mood.

It’s fascinating science and a very thought-provoking conversation that you can listen to now by clicking on the "Podcast" tab at the top of this page.

“It does not matter how slowly you go, as long as you do not stop.”

-Confucius

Comments