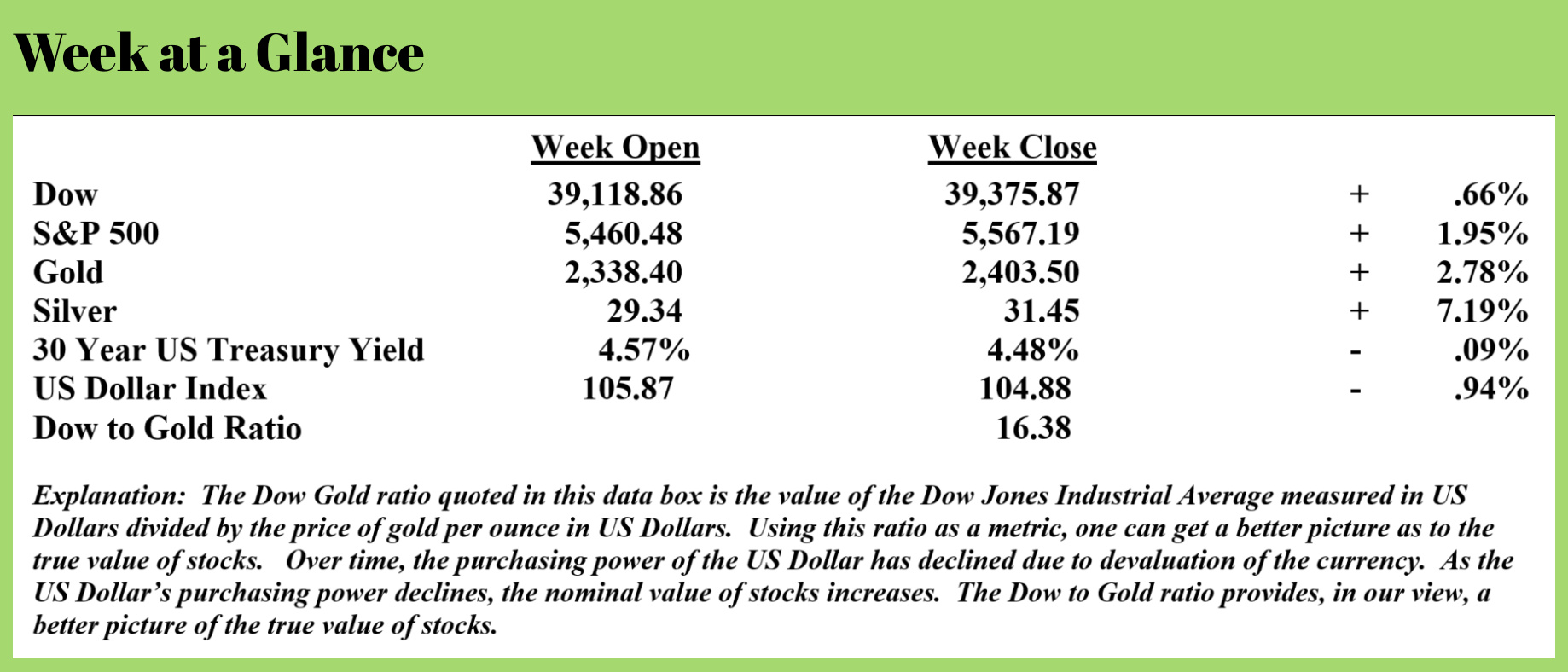

Weekly Market Update by Retirement Lifestyle Advocates

Weekly Market Update by Retirement Lifestyle Advocates

I was reading an article this past week about how the swimming pool industry is doing in the current economy. After reading the piece, it occurred to me that a ‘swimming pool indicator’ might indeed be a reliable leading economic indicator.

The article was published on “Axios” (Source: https://www.axios.com/2024/07/03/swimming-pools-us-economy-construction).

Seems, according to the article, that the swimming pool boom is over. Only 60,000 residential pools will be constructed this year, which is exactly half as many as in 2021. Pool Corp., a company that distributes pool equipment, estimated that pool construction would be down 20% from last year. And, should current trends continue, and the swimming pool market continues to weaken further, there could be fewer pools built than were constructed during the Great Recession year of 2009. That was immediately following a housing bust.

Interestingly, one can find evidence of the wealth gap in the swimming pool market as well. The “Axios” piece referenced above reported that higher-end pools with fancy waterfalls or decorative tiling are selling fine. It’s demand for lower end pools that is slowing.

This all makes sense when you consider it.

First, higher-end swimming pool purchasers tend to pay cash for their purchase, while lower-end pools are more likely to be financed. Much higher interest rates have significantly increased financing costs for all pay-over-time purchases, including swimming pools.

Second, inflation has consumed a lot more of the discretionary purchasing power of American households. There are many households that can simply no longer afford another payment since the cost of necessities is much higher than just a few years ago.

Third, since pools are often added when a new home is purchased and since new home sales are down, it follows that pool sales would also be down.

Fourth, inflation has made the cost of constructing a swimming pool more expensive. According to the same “Axios” article, the average pool cost went from approximately $40,000 pre-pandemic to somewhere between $65,000 and $70,000 presently.

Mirroring the price reduction trend that is occurring in the fast-food industry, many swimming pool companies and pool equipment companies are now offering hefty discounts to help spur sales.

Based on the swimming pool industry, it seems that the US economy is heading for or is already in a recession, and inflation is still taking its toll on living standards.

“The Epoch Times” recently ran a story on a report published by Bankrate (Source: https://www.theepochtimes.com/business/3-in-4-americans-say-theyre-not-financially-secure-new-report-shows-5678785) that found three out of four Americans felt they were not financially secure. This from that article:

According to a new Bankrate report, three in four Americans say they are not financially secure, and feel the need to make more money to attain an acceptable level of financial security. In the study YouGov, Americans said they needed to make $186,000 on average to feel financially secure – more than twice the $79,209 the Census Bureau reported the average full-time worker made in 2022.

Of the 75 percent who said they weren’t financially secure, 45 percent said they believed they would reach financial security one day, while 30 percent said they never expect to be financially secure.

The report said that older generations believed themselves less financially secure than younger generations.

Forty-two percent of baby boomers aged 60 to 78 and 37 percent of Gen Xers aged 44 to 59 said they were not financially secure – and didn’t think they ever would be. This compares to 12 percent of millennials aged 28 to 43 and 13 percent of Gen Z aged 18 to 27.

Younger generations were more likely to say they were not financially secure, but they would be one day – including 64 percent of Gen Z, 53 percent of millennials, 48 percent of Gen Xers, and 26 percent of baby boomers.

“Life always seems like it’d be better with just a little more money to spare,” Bankrate analysis Sarah Foster said of the report’s findings. “That’s even more true when the items Americans both need and want have been climbing in price. In the four years since the pandemic, comfort is no longer a commodity, but a financial privilege, appearing to only be afforded to those wealthy enough to ‘eat’ the impact of inflation.”

Six percent of survey respondents said they currently earn the annual income they need to feel financially secure, while 37 percent said they were less likely to earn a large enough salary to feel financially secure in their lifetime.

Of those earning more than $100,000 a year, 49 percent said they were optimistic they would be financially secure one day, while only 34 percent of those who made less than $50,000 were similarly optimistic.

Furthermore, Americans said they would need to make $520,000 to feel rich and financially free in the new report – up 8 percent from last year’s $483,000.

Inflation has impacted these numbers: Americans see prices rising and know they need more income to cover basic expenses. The Bureau of Labor Statistics calculates that inflation has caused a price increase of 21 percent since 2020, while the USDA says food prices have risen 25 percent, and US government data shows a 41 percent increase in gas prices.

As I have discussed in past issues of “Portfolio Watch” and on my RLA Radio program, the government’s estimates of inflation do not reflect inflation reality. One need only look at private inflation trackers like The Chapwood Index or ShadowStats.com to see what the actual inflation rate is.

As Ludwig von Mises so accurately stated, inflation is not a phenomenon; inflation is a policy. Deficit spending of $2.4 trillion this year creates inflation of 8% to 10% per year. Political rhetoric doesn’t change economic reality or the budget math.

But, then again, it’s not unusual for policies promulgated by politicians and bureaucrats to lead to unintended consequences. I devoted a chapter in my “Economic Consequences” book to this very topic.

Now, as a result of more policies put forth by short-sighted, pandering politicians, you can get ready to say goodbye to your free bank checking account. Chase Bank just announced the bank is ready to implement new charges for services that are now provided for free if new proposed government regulations take effect. This from “Zero Hedge’ (Source: https://www.zerohedge.com/markets/head-chase-bank-warns-customers-era-free-checking-likely-over):

The 'problem-solving' elites in Washington, DC, who advocate interventionist policies and overregulate the economy into oblivion, often cause unintended consequences. The latest example comes from the head of America's largest retail bank, which has a warning for its 86 million customers: The era of free checking is likely over.

Marianne Lake, head of Chase Bank, a division of JPMorgan Chase, was quoted by The Wall Street Journal as saying the bank is preparing to charge customers for now-free services, including checking accounts and wealth-management tools, if new rules pushed by politicians in Washington are enacted. These rules include capping overdrafts and late fees.

"The changes will be broad, sweeping, and significant," Lake said, adding, "The people who will be most impacted are the ones who can least afford to be, and access to credit will be harder to get."

Agencies such as the Consumer Financial Protection Bureau have proposed an $8 cap on late credit card payment fees and a $3 cap on over-drafting fees. There are also talks of placing limitations on debit card fees and the amount banks can charge CashApp and Venmo for accessing and using their customers' data.

In March, the CFPB passed a rule capping credit card late fees, but a series of bank industry groups sued to stop it before it became law. The law is now pending an appeal before a judge.

Even though the credit card late fee cap is in the hands of a court, some credit card companies are already preparing to pass costs to their respective customer bases.

"Chase has already sketched out plans to ratchet up interest rates and take a more conservative approach to underwriting credit card loans, according to an investor presentation," according to WSJ.

Dan Goerlich, a consulting partner at PricewaterhouseCoopers who advises banks, noted that mega banks will "make up for a dent in consumer banking revenues with profit from their wealth management and investment banking arms."

This week’s RLA radio program features an interview that I conducted with Mr. Murray Gunn, analyst at Elliott Wave International. I get Murray’s forecast for world markets and have a fascinating conversation with him about the predictive science of socionomics.

The radio program is available now by clicking on the "Podcast" tab at the top of this page. The weekly Headline Roundup newscast is also posted there. If you haven’t yet done so, check out all the free resources available here on our website.

“Go fast enough to get there, but slow enough to see.”

-Jimmy Buffet

Comments