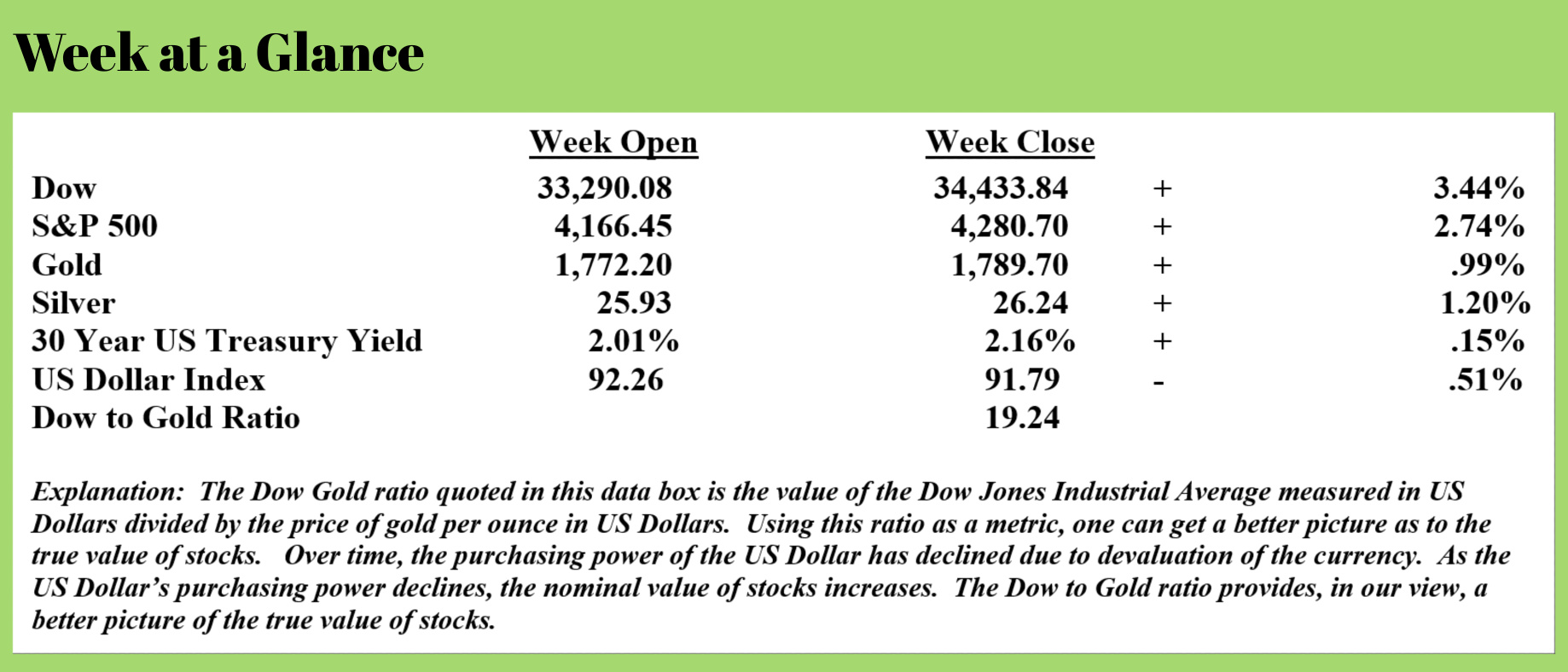

Weekly Market Update by Retirement Lifestyle Advocates

Weekly Market Update by Retirement Lifestyle Advocates

As I have suggested previously, the economic climate and the policy response to COVID (massive money creation) will change the perspective that many Americans have about retirement.

An article published by the Foundation for Economic Education (Source: https://fee.org/articles/survey-1-in-3-americans-to-postpone-retirement-after-lockdowns/) last week reported on the results of a survey that found one in three American workers who were thinking about retirement have now decided to delay their retirement plans.

This is a 180-degree turnaround from retirement numbers in the calendar year 2020 which saw more than 3 million baby boomers retire, a number that was about double the number of boomers retiring in 2019.

This from the article (emphasis added):

The COVID-19 pandemic saw a retirement surge in 2020, with more than 3.2 million baby boomers retiring—more than double the previous year.

New evidence, however, says a stunning number of Americans are preparing to do the opposite: delaying their Golden Years because of the financial hit they took during the pandemic.

“[A] study from Age Wave and Edward Jones finds that about 1 out of every 3 Americans who are planning to retire now say that will happen later due to Covid-19,” CNBC reports.

The poll, a survey of 2,042 adults conducted in March, estimates that 69 million Americans say their retirement plans have changed since March 2020.

The article also references a survey from last December that found approximately 22 million Americans had ceased making contributions to their retirement accounts. Four months later, in April of this year, only 8 million of those Americans had resumed making contributions to their retirement accounts meaning 14 million had not resumed contributions.

Another survey cited in the article conducted by Survey Monkey in January of this year found that 46 million Americans had their personal savings wiped out in 2020 implying that the reason many of these folks with retirement dreams are simply not in a position to resume contributions to their retirement accounts.

The lockdown response to COVID was far more devastating to those approaching retirement than to those who were already retired. The CNBC report noted above states “pre-retirees were more negatively impacted by the pandemic compared to retirees, 44% versus 22%, respectively.”

The reality is that the response to the pandemic, at least from an economic perspective, was far more devastating to pre-retirees than the actual disease.

Let’s briefly examine the obstacles to a comfortable, stress-free retirement now facing someone with retirement dreams.

The massive government spending in response to the lockdowns imposed were funded through newly created currency. One look at the Federal Reserve’s balance sheet currently sees that the Fed has more than $8 trillion in assets. That $8 trillion is simply the amount of new currency the Fed has literally created to buy securities.

All this newly created money is now leading to a very predictable conclusion – inflation is rearing its head on a large scale making it more difficult for aspiring retirees to save and for many Americans to cover the cost of their basic living expenses. This from “MSN Money” (Source: https://www.msn.com/en-us/money/personalfinance/e2-80-98i-e2-80-99m-going-to-go-broke-e2-80-99-this-is-how-rising-inflation-feels-for-an-american-who-e2-80-99s-living-on-disability-insurance/ar-AALr5yj) (emphasis added):

Lately, just about everything is costing Todd Richardson more than it did before the pandemic.

He’s paying $2 more per pound of chicken wings, his cable and electricity bills have also gone up by $100 since before the coronavirus pandemic, and he’s anticipating that his landlord will raise his rent from $750 to $1,100.

But that’s not even the biggest shock to him.

“I can’t believe cat litter and food have gone up by $5. How could they even do that? It’s kitty litter and cat food for God’s sake,” he said.

Richardson, 56, is only able to save $110 each month if he’s lucky.

Richardson used to work as a home-care aide for elderly people, but after contracting Lyme disease three years ago, which left him partially immobilized and with permanent neurological damage, he was forced to quit.

He receives around $1,500 a month in Social Security Disability Insurance benefits — half of which goes toward paying rent for his one-bedroom apartment in Plymouth, N.H. He spends the rest on transportation, cat supplies, electricity, cable, and food after he exhausts $200 a month in food stamps.

Richardson lives with his girlfriend, who also relies on Social Security Disability Insurance, and two cats. “Before the pandemic, I could survive,” Richardson told MarketWatch. He found small ways to save money, such as buying 99-cents-per-pound chicken wings at Walmart and visiting a local food pantry. Those same wings now cost $2 more per pound.

Richardson’s situation is hardly unique — Americans across the board are paying more for goods and services than they have in more than a decade due to inflation.

While Mr. Richardson’s difficulties may not exactly mirror those of someone more affluent who is planning to retire, the concerns are the same.

Why retire when one doesn’t know how the purchasing power of one’s savings will be affected in the near future due to continued Fed money creation? The safer option is to continue to work and see how this all plays out.

A would-be retiree counting on Social Security benefits for much of their retirement income might be nervous to put themselves on a fixed income with adjustments for inflation that are more form than substance.

And, given that interest rates have been kept artificially low, retirees who would be logically looking for a more conservative investment approach during retirement are left with a conundrum. Maintaining a conservative approach to avoid losing significant investment assets during a stock market crash will, over time, see a portfolio lose purchasing power due to the huge gap between the real inflation rate and fixed interest available on a conservative investment vehicle.

According to John Williams at ShadowStats.com, the real inflation rate is presently about 13%. Interest available on a conservative, fixed interest investment is more than 10 percentage points lower. That puts retirees in a very precarious situation – take more risk than they should be taking to attempt to retain purchasing power or use a conservative investment knowing that should present policies continue, the future purchasing power of investments will be devastated.

An aspiring retiree planning for retirement using traditional strategies is choosing between two potentially ugly outcomes.

Interestingly, the surveys conducted reference the pandemic as the cause of the current economic problems when the reality is the response to the pandemic, namely lockdowns and massive money creation, that are the real culprits here.

A government operating with a balanced budget in a sound money system would have been able to react to COVID in a much different manner without the inflationary fallout that we are all presently experiencing.

That however was not the case.

Going into the pandemic, the government was already fundamentally broke. The Fed was already subsidizing much of the government’s deficit spending through money creation. The level of money creation since early 2020 has now simply gone off the charts.

It’s important to understand that there is a time lag between money creation and inflation. We are now seeing the inflationary results of last year’s money creation.

However, money creation hasn’t stopped. Politicians refuse to collectively realize that additional, new spending will add to the deficit, resulting in more money creation and add to the pain that many Americans are now feeling.

It’s a twisted irony that printing currency to help those in the population who need it actually ends up hurting those same people the most.

If you’re an aspiring retiree, consider using the Revenue Sourcing approach described in the book “Revenue Sourcing: A Retirement Planning Strategy for the Post-Pandemic Economy”.

This week’s RLA radio program features an interview with Mr. Michael Pento of Pento Portfolio Strategies.

Michael is a frequent commentator on all things economic and financial. I interview Michael about his view that inflation will be followed by deflation as early as next year.

The program is available to listen to now by clicking on the "Podcast" button at the top of this page.

“I can win any argument, on any topic against any opponent. People know this and steer clear of me at parties. Often, as a sign of their great respect, they don’t even invite me.”

-Dave Barry