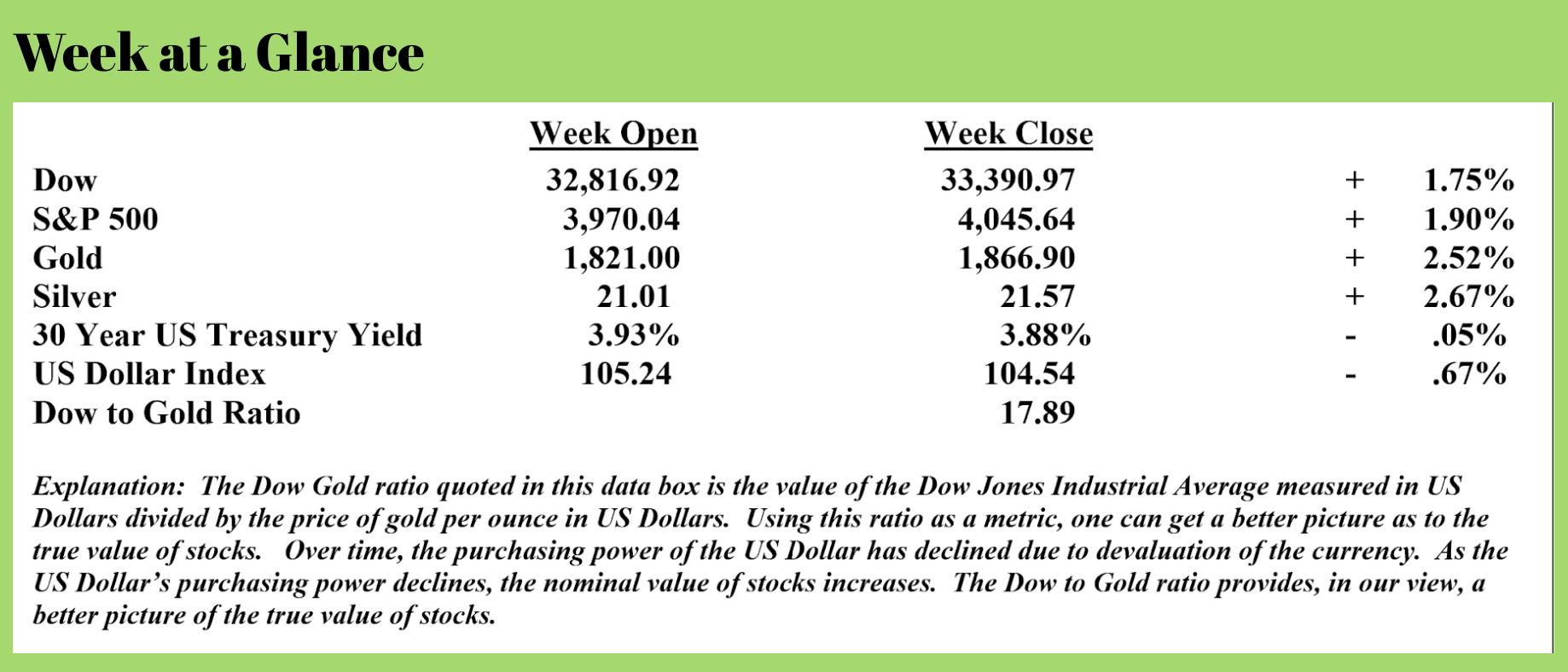

Weekly Market Update by Retirement Lifestyle Advocates

Weekly Market Update by Retirement Lifestyle Advocates

In last week’s “Portfolio Watch”, I discussed the inevitable outcome of government overspending and the central bank overprinting.

This outcome will be as ugly as it will be predictable in my view.

Eventually, inflation will give way to an ugly deflationary environment. In the meantime, we will probably see stagflation – rising consumer prices and falling asset prices. Professor Nouriel Roubini has a similar take. This from “Markets Insider” (Source: https://markets.businessinsider.com/news/stocks/nouriel-roubini-economy-recession-inflation-debt-market-crash-dr-doom-2023-3):

A "perfect storm" is brewing, and markets this year are going to get hit with a recession, a debt crisis, and out-of-control inflation, the economist Nouriel "Dr. Doom" Roubini said.

Roubini, one of the first economists to call the 2008 recession, has been warning for months of a stagflationary debt crisis, which would combine the worst aspects of '70s-style stagflation and the '08 debt crisis.

"I do believe that a stagflationary crisis is going to emerge this year," Roubini said Thursday in an interview with Australia's ABC.

With consumer inflation still sticky at 6.4%, Roubini said he estimated that the Federal Reserve would need to lift benchmark rates "well above" 6% for inflation to fall back to its 2% target.

That could spark a severe recession, a stock-market crash, and an explosion in debt defaults, leaving the Fed with no choice but to back off its inflation fight and let prices spiral out of control, he added. The result would be a steep recession, anyway, followed by more debt and inflation problems.

"Now we're facing the perfect storm: inflation, stagflation, recession, and a potential debt crisis," Roubini said.

He has remained ultrabearish on the economy, despite the market's growing hope that the US could skirt a recession this year.

Though more bullish commentators are making the case for a healthy rebound in the S&P 500, which fell 20% last year, Roubini has previously said the benchmark stock index could slide another 30% as investors battled extreme macro conditions.

"They will continue to go down," he said of stocks, pointing to the recent sell-off as investors priced in higher interest rates from the Fed. "The market is already correcting."

He urged investors to protect themselves by choosing inflation hedges, such as gold, inflation-indexed bonds, and short-term bonds. Those picks are likely to beat stocks and bonds, he said, which could suffer.

I believe Roubini is correct on a couple of counts.

Stocks will likely decline further in my view. One only needs to look at the Buffet Indicator to quickly conclude that despite last year’s decline in stock values, stocks remain heavily overvalued.

And, in order to tame inflation, as I have stated previously, real interest rates need to be positive – interest rates need to be higher than the inflation rate.

There are already signs of stagflation emerging. The real estate market is a good example. Wolf Richter, had this to say on real estate (Source: https://wolfstreet.com/2023/03/04/housing-bust-2-has-begun/):

The housing market in the United States has turned down, and in some big markets very dramatically so. Other markets lag a little behind.

That’s how it went during the last Housing Bust, that I now call Housing Bust #1. During Housing Bust #1, Miami, Phoenix, San Diego, Las Vegas, etc. were a little ahead; other places, like San Francisco were a little behind. In 2007, people in San Francisco thought they would be spared the housing bust they saw unfolding across the country. And then it came to San Francisco with a vengeance.

This time around, San Francisco and Silicon Valley, and the entire San Francisco Bay Area, are at the forefront, along with Boise, Seattle, and some others. In the San Francisco Bay Area, during the first 10 months of this housing bust, Housing Bust #2, the median house price has plunged faster than it did during the first 10 months of Housing Bust #1. That’s what we’re looking at. I’ll get into the details in a moment.

Across the US, home sales have plunged month after month ever since mortgage rates started to rise a year ago. In January, across the US, total home sales plunged by 37% from January last year. Sales plunged in all regions, but they plunged worst in the West, by 42% year-over-year, and the least worst, if I may, in the Midwest, by 33%. This is happening everywhere.

The median price of all types of homes across the US in January fell for the seventh month in a row, down over 13% from the peak in June. Some of the decline is seasonal, and some is not.

This drop whittled down the year-over-year gain to just 1.3%. At this pace, we will see a year-over-year price decline in February or March, which would be the first year-over-year price decline across the US since Housing Bust 1.

Active listings were up by nearly 70% from a year ago, though by historical standards they’re still low. Lots of sellers are sitting on their vacant properties and are holding them off the market, and are putting them on the rental market or are trying to make a go of it as vacation rentals. And they’re all hoping that “this too shall pass.”

“This too shall pass” – that’s the mortgage rates. The average 30-year fixed mortgage rate went over 7% late last year, then in January, it dropped, went as low as 6%, and the entire industry was breathing a sigh of relief. This was based on fervent hopes that inflation would just vanish, and that the Federal Reserve would cut interest rates soon, and be done with this whole nightmare.

But in early February came the realization that inflation wasn’t just going away. Friday’s inflation data confirmed that inflation is reaccelerating, that it already started the process of reacceleration in December. Some goods prices are down, but inflation in services spiked to a four-decade high. Services is nearly two-thirds of what consumers spend their money on. Inflation is very difficult to dislodge from services. The Federal Reserve is going to have its hands full dealing with this – meaning higher rates for longer.

And mortgage rates jumped again and on Friday were back to about 6.9%, according to the daily measure by Mortgage News Daily. Just a hair below the magic 7%.

And potential sellers are still sitting on their vacant properties, thinking: and this too shall pass.

So how many vacant homes are there? The Census Bureau tracks this. In the fourth quarter last year, there were nearly 15 million vacant housing units – so single-family houses, condos, and rental apartments. That’s over 10% of the total housing stock.

In 2022, the number of total housing units increased by over 1.3 million. If each housing unit is occupied on average by 2.5 people, that’s housing for 3.3 million more people than in the prior year. The US population hasn’t grown nearly that fast in 2022.

Ok, so now here are nearly 15 million vacant housing units. Of them, 11 million were vacant year-round. Some of the 11 million were being remodeled to be rented out, and others were for sale, and that’s the inventory we actually see, and there are other reasons why homes were vacant.

But 6.6 million homes were held off the market, for a variety of reasons, such as that the owners don’t want to sell the property at the moment.

If just 10% of these 6.6 million homes that are held off the market show up on the market, it would double the total number of active listings. If 20% of these homes show up on the market, it would trigger an enormous glut.

This is the shadow inventory. It can emerge at any time. And during Housing Bust 1, this shadow inventory that suddenly emerged created the biggest housing glut ever.

As I noted last week, history teaches us that excessive debt levels lead to deflation.

This time will ultimately be no different.

Deflation will at some point, become the prevalent economic force. In the meantime, expect stagflation.

That will be more bad news for stocks and real estate as well as consumer prices.

The best advice that I can offer is to have some of your assets that will be protected from a prolonged decline in stocks and real estate and other assets that will perform well in an inflationary environment.

The radio program this week features an interview with Jeffrey Tucker, founder of the Brownstone Institute.

Jeffrey and I discuss the current economic forecast as well as what we’ve learned from the COVID-related economic lockdowns. It’s a thought-provoking conversation that you won’t want to miss.

You can listen to the show now by clicking on the "Podcast" tab at the top of this page.

“Do you know who will be in charge of healthcare? The IRS. You thought getting audited was bad? Wait until your next prostate exam.”

-Jay Leno

Comments