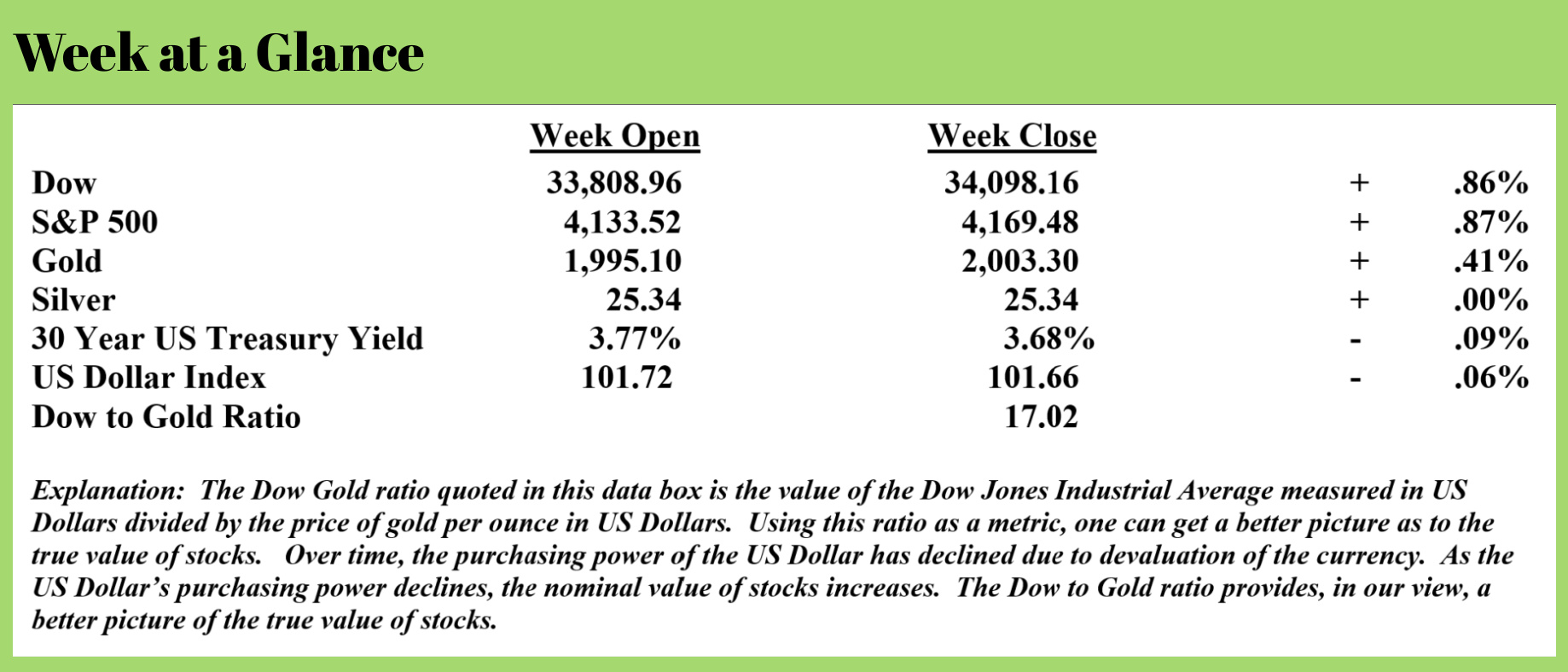

Weekly Market Update by Retirement Lifestyle Advocates

Weekly Market Update by Retirement Lifestyle Advocates

Did you hear about the latest lunacy out of Washington?

Mark my words; it will create yet another headwind for a real estate market that is beginning to flounder without this change.

Seems that homebuyers with good credit and larger down payments will now pay more in mortgage origination fees than poorly qualified, more marginal home buyers.

Really.

You can’t make this stuff up.

This from “The New York Post” (Source: https://nypost.com/2023/04/16/how-the-us-is-subsidizing-high-risk-homebuyers-at-the-cost-of-those-with-good-credit/)

A little-noticed revamp of federal rules on mortgage fees will offer discounted rates for home buyers with riskier credit backgrounds — and force higher-credit homebuyers to foot the bill, The Post has learned.

Fannie Mae and Freddie Mac will enact changes to fees known as loan-level price adjustments (LLPAs) on May 1 that will affect mortgages originating at private banks nationwide, from Wells Fargo to JPMorgan Chase, effectively tweaking interest rates paid by the vast majority of homebuyers.

The result, according to industry pros: pricier monthly mortgage payments for most homebuyers — an ugly surprise for those who worked for years to build their credit, only to face higher costs than they expected as part of a housing affordability push by the US Federal Housing Finance Agency.

“It’s going to be a challenge trying to explain to somebody that says, ‘I worked my whole life for high credit and I’ve put a lot of money down and you’re telling me that’s a negative now?’ That’s a hard conversation to have,” one worried Arizona-based mortgage loan originator told The Post.

“It’s unprecedented,” added David Stevens, who served as Federal Housing Administration commissioner during the Obama administration. “My email is full from mortgage companies and CEOs [telling] me how unbelievably shocked they are by this move.”

The tweaks could further complicate the strenuous mortgage application process and add more pressure on a core segment of buyers in a housing market already in the midst of a major downturn, the experts added. The average 30-year mortgage rate is hovering at 6.27% as of last week — up from about 5% one year ago and more than twice as high as it was two years ago, according to Freddie Mac data.

Under the new rules, high-credit buyers with scores ranging from 680 to above 780 will see a spike in their mortgage costs – with applicants who place 15% to 20% down payment experiencing the biggest increase in fees.

“This was a blatant and significant cut of fees for their highest-risk borrowers and a clear increase in much better credit quality buyers – which just clarified to the world that this move was a pretty significant cross-subsidy pricing change,” added Stevens, who is also the former CEO of the Mortgage Bankers Association.

LLPAs are upfront fees based on factors such as a borrower’s credit score and the size of their down payment. The fees are typically converted into percentage points that alter the buyer’s mortgage rate.

Under the revised LLPA pricing structure, a home buyer with a 740 FICO credit score and a 15% to 20% down payment will face a 1% surcharge – an increase of 0.750% compared to the old fee of just 0.250%.

When absorbed into a long-term mortgage rate, the increase is the equivalent of slightly less than a quarter percentage point in mortgage rate. On a $400,000 loan with a 6% mortgage rate, that buyer could expect their monthly payment to rise by about $40, according to calculations by Stevens.

Meanwhile, buyers with credit scores of 679 or lower will have their fees slashed, resulting in more favorable mortgage rates. For example, a buyer with a 620 FICO credit score with a down payment of 5% or less gets a 1.75% fee discount – a decrease from the old fee rate of 3.50% for that bracket.

When absorbed into the long-term mortgage rate, that equates to a 0.4% to 0.5% discount.

The FHFA-ordered overhaul of LLPAs affects purchase loans, limited cash-out refinances and cash-out refinance loans.

Yep, you read that correctly. If you have a credit score of 770 and have 20% down, you’ll now pay more for your mortgage, while someone with a 600 credit score, up to their neck in debt, will pay less.

This will be an additional drag on real estate moving ahead in a real estate market that is already struggling. While residential real estate is slowing, the commercial real estate market is really hurting, with more pain on the horizon.

This from “USA Today” (Source: https://www.msn.com/en-us/money/realestate/commercial-real-estate-is-headed-for-a-crisis-worse-than-2008-morgan-stanley-analysts-say/ar-AA19Bwyd)

In February, a PIMCO-owned office landlord defaulted on an adjustable rate mortgage on seven office buildings in California, New York and New Jersey when monthly payments rose due to high interest rates.

Brookfield, the largest office owner in downtown Los Angeles, that month chose to default on loans on two buildings rather than refinance the debt due to weak demand for office space.

They are a bellwether for what is likely to come, as more than half of the $2.9 trillion in commercial mortgages will be up for refinancing in the next couple of years, according to Morgan Stanley.

“Even if current rates stay where they are, new lending rates are likely to be 3.5 to 4.5 percentage points higher than they are for many of CRE’s existing mortgages,” wrote Morgan Stanley Chief Investment Officer Lisa Shalett, in a recent report.

Even before the collapse of Silicon Valley Bank and Signature Bank in March, the commercial real estate market was dealing with a host of challenges including dwindling demand for office space brought on by remote work, increased maintenance costs and climbing interest rates.

With small- and medium-size banks accounting for 80% of commercial real estate lending, the situation might soon get worse, says experts.

Commercial property prices could fall as much as 40% “rivaling the decline during the 2008 financial crisis,” forecast Morgan Stanley analysts.

“These kinds of challenges can hurt not only the real estate industry but also entire business communities related to it,” says Shalett.

While the Morgan Stanley analysts are forecasting a 40% decline in commercial real estate values, I’d forecast more downside than that. With nearly $3 trillion in commercial mortgages in existence, a 4% increase in interest rates on mortgage renewals on properties that may already be having difficulty cash flowing could be the difference between surviving and foreclosure.

According to the “USA Today” article, the commercial real estate sector is already in trouble. Commercial real estate includes hotels, office buildings and shopping centers.

Not surprisingly, office space is having the most difficulty. 44% of office building loans were in delinquency in 2021 when measured by volume.

That is simply a huge number.

This will undoubtedly lead to additional problems in the banking sector.

The radio program this week features an interview with economic and currency author. Mr. John Rubino.

John comments on the current state of the economy, the future of the US Dollar, and investing opportunities moving ahead in light of the significant economic change that he anticipates.

You can listen to the shower now by clicking on the "Podcast" tab at the top of this page.

“Facts are stubborn things, but statistics are more pliable.”

-Mark Twain

Comments