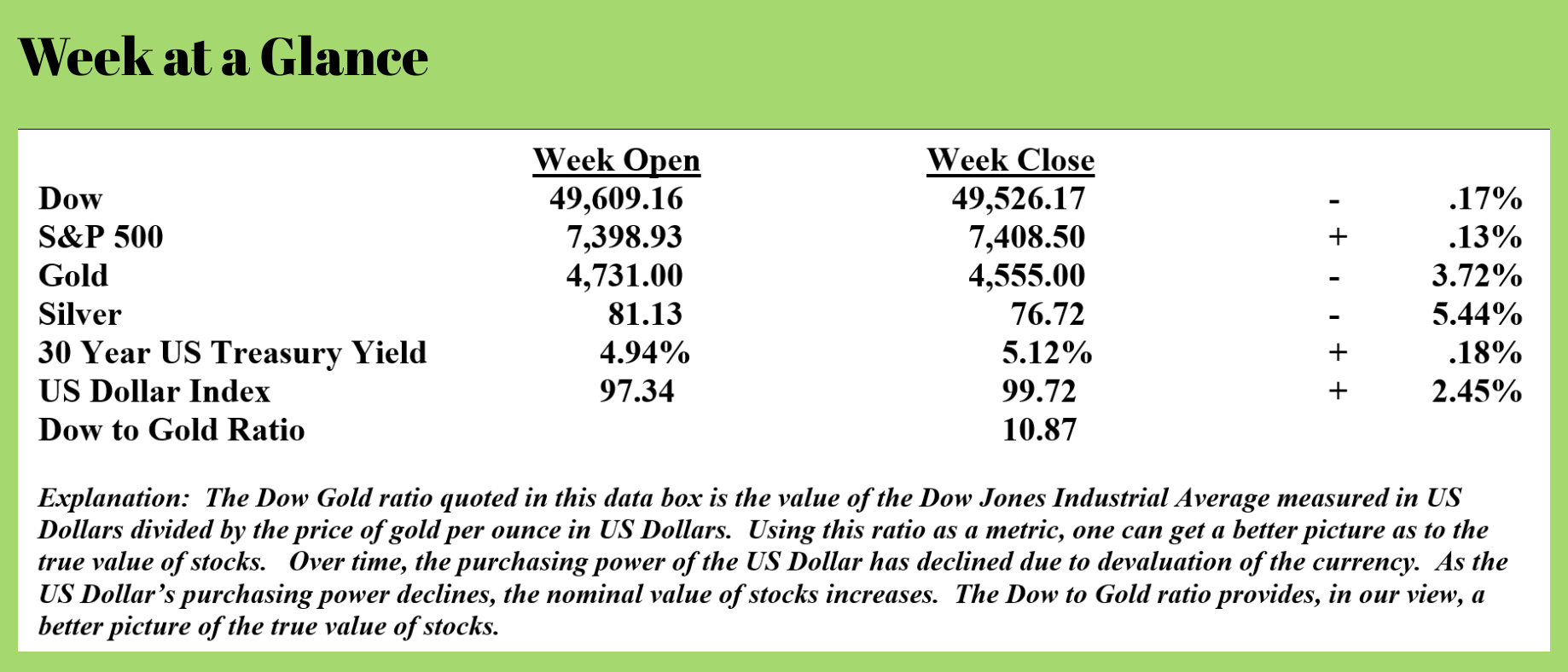

Weekly Update from RLA Tax and Wealth Advisory

Weekly Update from RLA Tax and Wealth Advisory

By: Dennis Tubbergen

Bond Market Trouble Looming?

Last week, the yield on the 30-Year US Treasury Bond surged through the 5% level to finish the week with a yield of 5.12%.

There are two reasons that bond yields move higher. One, because the borrower, in this case, the US Government, is less creditworthy. That is certainly the case with the US Government, with the official national debt approaching $40 trillion. The outlook for US Government finances is bleak, with $2 trillion annual operating deficits for as far as the eye can see.

The second reason that yields spike is from inflation fears. If one buys $10,000 of US Treasuries yielding 4%, that’s $400 per year in interest income. If your favorite bottle of wine costs $40, then the interest earned on the bonds will buy 10 bottles of your favorite wine.

The second reason that yields spike is from inflation fears. If one buys $10,000 of US Treasuries yielding 4%, that’s $400 per year in interest income. If your favorite bottle of wine costs $40, then the interest earned on the bonds will buy 10 bottles of your favorite wine.

Now, let’s assume that due to inflation, your favorite bottle of wine now costs $60. Now the interest on your bond portfolio won’t even buy 7 of your favorite bottles. Now, to combat the negative effects of inflation, you may demand more interest on the same investment and, if you can’t get it, you might begin to look for alternative investment options.

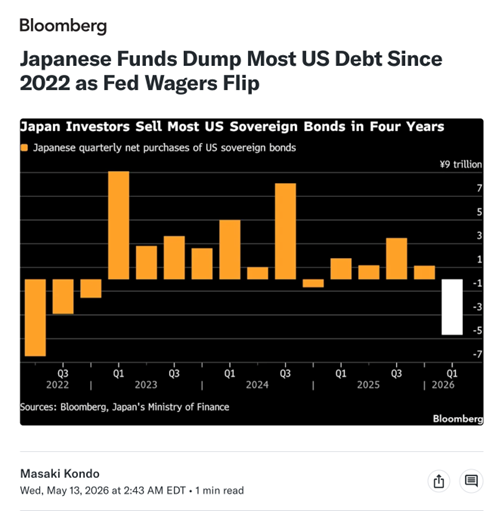

Last week, the country of Japan quietly dumped a large amount of US Treasury holdings. Look at this chart from Bloomberg illustrating that Japan sold more US debt than at any time since 2022.

In the case of US Treasuries, the recent spike in interest rates is likely due to both US creditworthiness and inflation concerns. Bottom line, interest rates will have to continue to rise over time to attract investors to US Government bonds. We are keeping our US Government bond focus on short-term bills.

Foreclosures Spike

Foreclosure filings rose 18%year-over-year in the month of April (Source: https://www.dailymail.com/real-estate/article-15815623/banks-foreclosures-housing-crisis-america.html), signaling that more homeowners are struggling to maintain their homes.

ATTOM, a real estate analytics firm, released data that confirmed 42,430 properties nationwide received foreclosure filings in April 2026. The number of foreclosure filings fell slightly from the month of March, but was much higher year-over-year.

The Chief Executive Officer of ATTOM, Rob Barber, noted, “Foreclosure activity continued its gradual trend higher in April. The year-over-year increases suggest lenders may be working through distressed inventory, and higher borrowing costs and affordability challenges impact some homeowners.”

Foreclosure starts were also up year-over-year by 12%.

The State of Delaware led the nation in foreclosure filings, with 1 in every 1739 properties receiving a foreclosure notice in April. South Carolina was second in foreclosure filings, followed by Florida in third place. Indiana and Illinois rounded out the top five states.

Charitable Giving and Your Taxes

Beginning this year, in 2026, the tax deduction rules around charitable gifts have changed.

In this issue, I’ll give you a brief overview, as I understand these new rules; however, always seek advice from a qualified professional for your individual financial situation.

The first change, and one that likely applies to many readers of “Portfolio Watch,” is charitable contribution deductibility for taxpayers who take a standard deduction on their 1040 (as opposed to itemizing deductions).

Since the standard deduction is now generous when compared to past years, $16,100 for single taxpayers and $32,200 for married taxpayers filing jointly, many taxpayers who gave to charity couldn’t utilize those charitable contributions on their tax return since the total of their itemized deductions did not exceed the standard deduction amount.

For these taxpayers, there is some good news this year – at least a small amount of good news. Taxpayers who take a standard deduction can now deduct some charitable contributions in addition to the standard deduction amount. Single taxpayers can deduct up to $1,000 in additional contributions, and married taxpayers can deduct up to $2,000 in additional contributions. Contributions to donor-advised funds are excluded.

In 2026, taxpayers who itemize their deductions won’t be able to deduct charitable contributions from dollar one. Only charitable contributions that exceed .5% of a taxpayer’s adjusted gross income can be deducted.

A taxpayer with $200,000 in adjusted gross income will not be able to deduct the first $1,000 in charitable contributions made in a year but will be able to begin deducting charitable contributions at $1,001 in donations. To be clear, a taxpayer with an adjusted gross income of $200,000 annually who makes a $2,000 contribution to charity will be able to deduct $1,000, or the amount in excess of .5% of adjusted gross income.

Deductions for charitable gifts are now capped at 35% of income. If you are in the top tax bracket of 37%, a charitable contribution can only be deducted at 35%.

And, qualified charitable distributions, or QCD’s, can be made directly from a retirement account to a qualified charity if the taxpayer has attained age 70½ in an amount up to $111,000 per year. A QCD has no tax consequences, allowing a taxpayer to take money out of a retirement account with zero tax.

RLA Radio

The RLA radio program this week features an interview that I did with Mr. Karl Deninger.

The interview is now posted. Click on the "Podcast" tab at the top of this page to listen, or you can find it on your favorite podcast channel.

Quote

“Camping is nature’s way of promoting the motel business.”

-Dave Barry

Comments