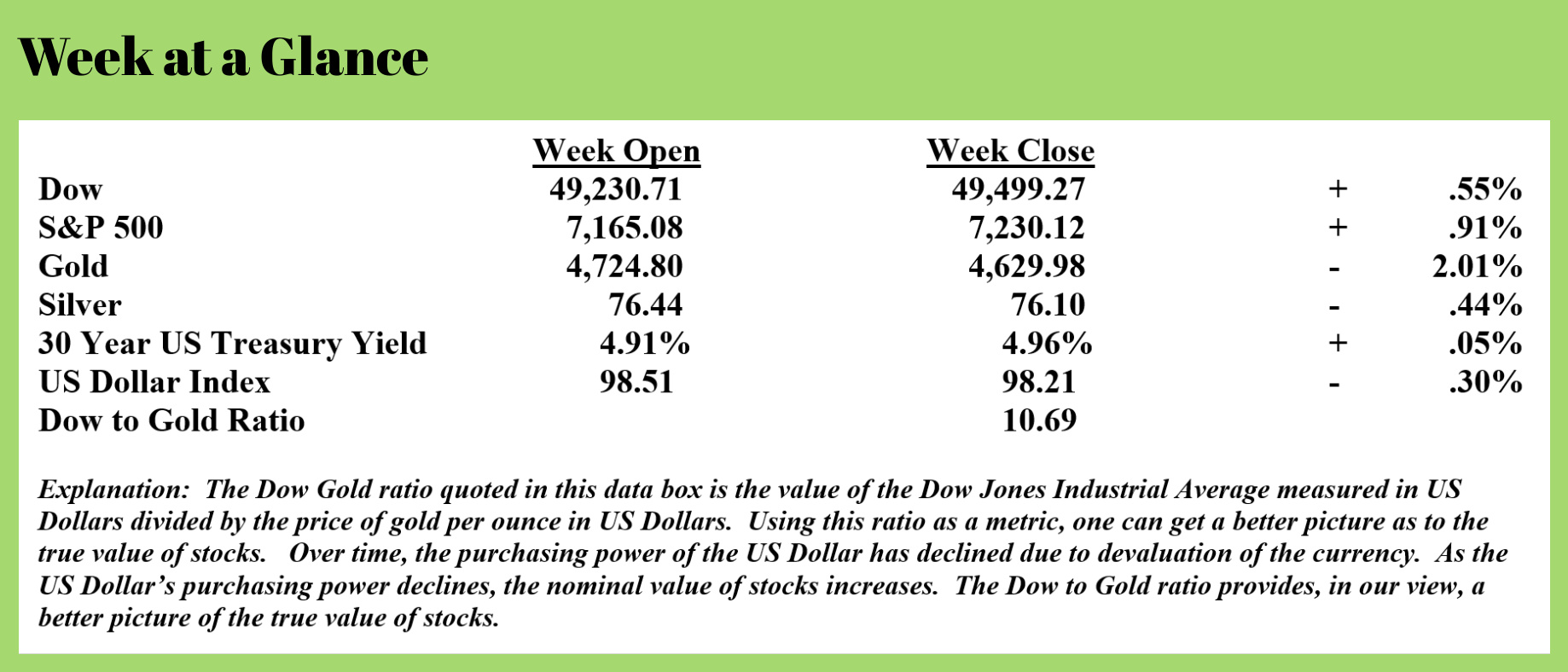

Weekly Update from RLA Tax and Wealth Advisory

Weekly Update from RLA Tax and Wealth Advisory

By: Dennis Tubbergen

Did the Fed Just Admit Its Monetary Policy Caused the Wealth Gap?

As I’ve previously stated in this publication, the consumer spending-dependent US economy has been relying on spending from the top income earners and the wealthiest Americans to give the outward appearance that the economy is reasonably healthy.

The Federal Reserve Bank of New York released research last week in which the central bank indirectly admits that the inflationary monetary policies that it has been pursuing have created a “K-Shaped” economy with most spending coming from the affluent, while lower-income Americans and those with few assets are struggling with persistent inflation and now much higher fuel prices.

The Federal Reserve Bank of New York posted this recently: “Reliance on a single segment of the economy has important implications for spending growth and its fragility, as well as for economic vulnerability and policy.”

Translation: If the affluent quit spending, the economy is likely toast.

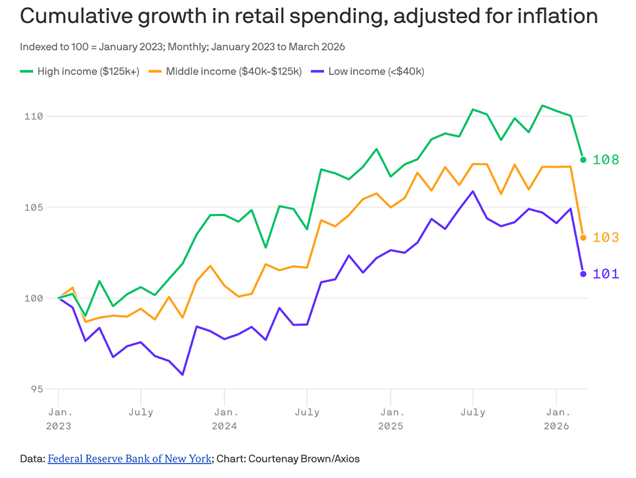

This chart shows that the ‘toast’ moment may be quickly approaching.

This chart shows that the ‘toast’ moment may be quickly approaching.

The green line on the chart tracks the spending of Americans earning more than $125,000 per year. The chart begins in January of 2023. Notice that spending was uptrending through January of this year.

The gold line on the chart illustrates the spending of middle-class consumers. It is just 3% higher over the last three years (the chart begins with a reference value of 100, and the reference value is now 103).

Low-income Americans have seen their spending increase just 1% over the past three years.

Note that spending among all age groups has dropped precipitously since the beginning of this year.

If this trend continues, it is definitely recessionary.

Inflation Heating Up as New Fed Chair Takes Over

The Fed’s preferred inflation measure, PCE or personal consumption index was up 3.5% from February to March (Source: https://www.bea.gov/data/personal-consumption-expenditures-price-index). That’s far above the Fed’s long-stated, arbitrarily selected inflation target of 2%.

Given that PCE is nearly double the Fed’s target, what can we expect from the incoming Fed Chair, Kevin Warsh?

Warsh’s written answers to the Senate give us a strong indication as to where monetary policy goes from here. Warsh stated in these written answers that he does not think inflation statistics are accurate. (Source: https://rubino.substack.com/p/lawrence-lepard-new-fed-chair-new). In his testimony, Warsh suggested using a ‘trimmed mean’ method to calculate inflation. This method throws out outlier prices, which results in a lower reported inflation rate.

If you’re reading between the lines and see this as a justification for lower interest rates and still easier monetary policy, I agree with you. Lower interest rates and more currency creation, as seen after the financial crisis and at the time of COVID, could very likely set off another easy money credit expansion and perhaps even more of an asset bubble.

But the Fed is between the proverbial rock and a hard place. The US Government simply can’t afford to finance and refinance it’s ever- growing debt at higher interest rates.

The problem is that despite the Fed cutting the Fed Funds rate, market interest rates have moved higher. They always do in an inflationary environment.

The 30-Year US Treasury Bond yield is now, for all practical purposes, at 5%. Short-term bills are now between 3.5% and 4% on treasury maturities from 4 weeks to 26 weeks.

A fed rate cut and more easy money policies will, in my view, further fuel inflation and lead to higher interest rates, further exacerbating the Fed’s problem.

At that point, the Fed may elect to take a page from the playbook of the Japanese central bank and pursue a policy of yield curve control.

Yield curve control is a policy that has the Fed creating currency from thin air to create artificial demand for US Treasuries should interest rates exceed a predetermined level.

For example, if the Fed decides that the ceiling on short-term US Treasury yields will be 4%, then should interest rates move above that level, the Fed will step in and buy the Treasuries, creating demand to keep interest rates lower and more manageable.

The obvious problem here is that creating currency from thin air is inflationary, further feeding this cycle that feeds on itself.

The answer to the persistent inflation problem is a balanced federal budget. With the DOGE exercise now long concluded with no impactful results and with $2 trillion federal budget deficits for as far as the eye can see, a proactive solution to this problem is unlikely in my view.

That means easy-money policies will continue until they can’t. Until then, look for inflation to continue to heat up.

Investing accordingly will, from my vantage point, not only be advisable, but perhaps vitally important.

RLA Radio

The RLA radio program this week features an interview I did with Mr. Charles Hughes, in which we discuss whether the Federal Reserve can fight deflationary pressures without reigniting inflation.

The interview is now posted and available by clicking on the "Podcast" tab at the top of this page.

Quote

“Fix the money, fix the world.”

-Lawrence Lepard

Comments