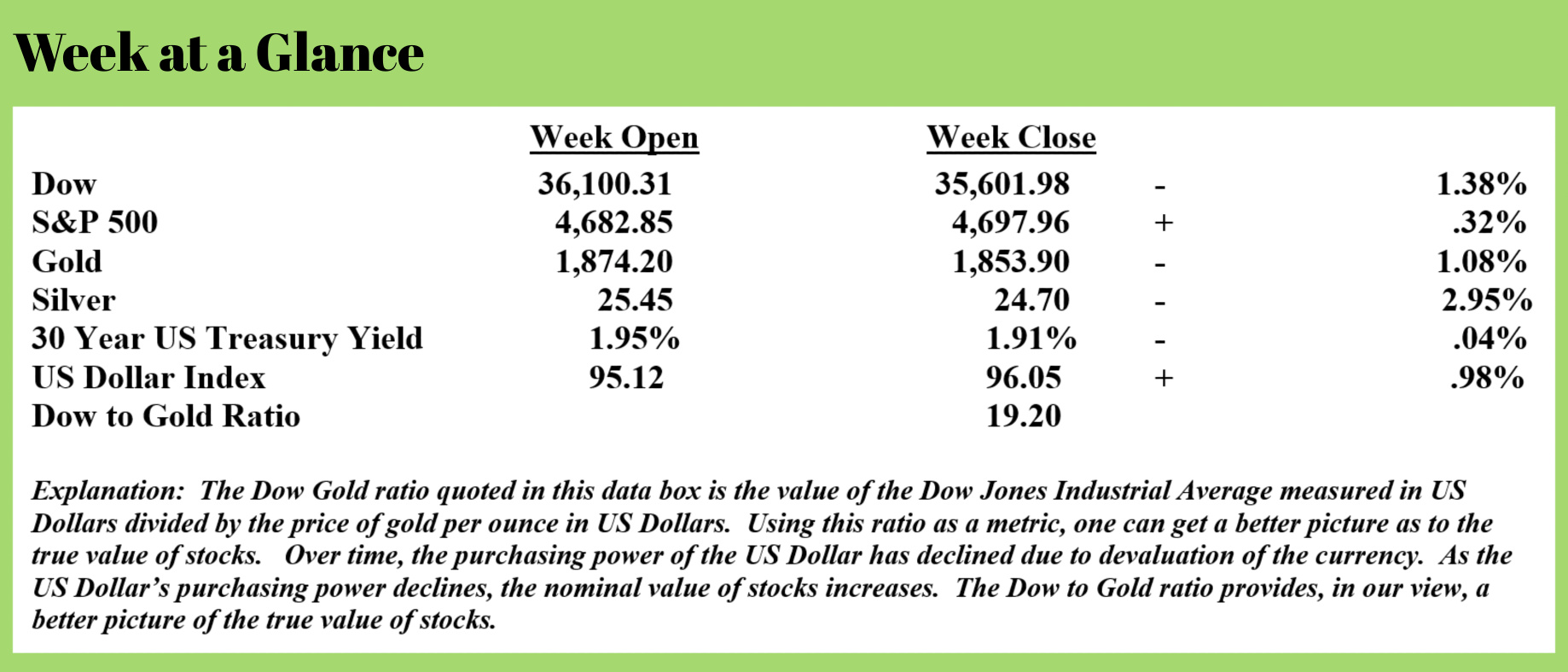

Weekly Market Update by Retirement Lifestyle Advocates

In this weekly publication, I comment frequently on Federal Reserve policies largely because Fed policy is the primary driver of economic and investing conditions.

Over the past dozen years or so, the Fed has created currency literally from thin air, a process known as quantitative easing, and has kept interest rates at artificially low levels.

History teaches us these policies create a prosperity illusion for a while but, in the end, reality emerges and the price for such reckless policy is paid.

An astute observer who is doing his or her own research can now see the beginning of reality emerging. One such reality is the extremely difficult position in which pension managers now find themselves as a result of the Fed’s low interest rate policy.

During this week’s RLA Radio Program, I discuss this in detail.

There are two types of pension plans – a defined contribution plan and a defined benefit plan. A defined contribution plan is the retirement plan with which you are probably most familiar. One example of such a plan is a 401(k) plan. This type of pension plan is known as a defined contribution plan because the contribution to the plan, or investment in the plan is what is ‘defined’ or determined.

For example, in a 401(k) plan, you determine the contribution, and the ultimate benefit received at retirement is dependent on the amount of the contribution and the investment results of the plan.

The other type of retirement plan is a defined benefit plan. This is most commonly a pension plan where the monthly benefit at retirement is defined. The plan is then funded by the employer to an extent as to ensure that the plan can meet the monthly retirement payment obligations to the retiree.

There are several variables that determine the level of employer funding to a defined benefit plan; the number of years until the covered employee retires, the amount of monthly retirement income the employee is to receive (usually determined by a formula involving a number of years of service and employee salary) and the investment results of the plan.

As you might imagine, pension assets need to be invested in a way as to maximize safety as well as returns. In a low interest rate environment like the one we’ve seen for the past 12 years or so, it’s exceptionally difficult for a pension fund management team to get reasonable returns and maintain safety.

This is an adverse side effect of the Fed’s artificially low interest rate policy and it’s now beginning to take its toll on pensions in earnest. So much so that some pension plans are now forced to either fund the pension plan to a greater extent to compensate for lower interest rates or subject plan assets to more investment risk.

This past week, “The Wall Street Journal” published an article that reported the nation’s largest pension fund, CALPERS, has now decided to take more investment risk to attempt to get the pension plan closer to being more fully funded.

The article headline and an excerpt follow (Source: https://www.wsj.com/articles/retirement-fund-giant-calpers-votes-to-use-leverage-more-alternative-assets-11637032461?mod=Searchresults_pos2&page=1):

The board of the nation’s largest pension fund voted Monday to use borrowed money and alternative assets to meet its investment-return target, even after lowering that target just a few months ago.

The move by the $495 billion California Public Employees’ Retirement System reflects the dimming prospects for safe publicly traded investments by households and institutions alike and sets a tone for increased risk-taking by pension funds around the country.

Without changes, Calpers said its current asset mix would produce 20-year returns of 6.2%, short of both the 7% target the fund started 2021 with and the 6.8% target implemented over the summer.

“The times have changed since this portfolio was put together,” said Sterling Gunn, Calpers’ managing investment director, Trust Level Portfolio Management Implementation.

Board members voted 7 to 4 in favor of borrowing and investing an amount equivalent to 5% of the fund’s value, or about $25 billion, as part of an effort to hit the 6.8% target, which they voted not to change. The trustees also voted to increase riskier alternative investments, raising private-equity holdings to 13% from 8% and adding a 5% allocation to private debt.

Borrowing money to increase returns allowed Calpers to justify the 6.8% target while maintaining a more-balanced asset mix, concentrating less money in public equity, and putting more in certain fixed-income investments, fund staff and consultants said.

A staff presentation noted, however, that the use of leverage “could result in higher losses in certain market conditions,” a possibility that raised concerns for board member Betty Yee, the California state controller.

“Ultimately the question is, does the risk outweigh the benefit?” Ms. Yee asked.

Retirement funds around the U.S. have been pushing into alternative assets such as real estate and private debt to drive up investment returns to pay for promised future benefits. Funds have hundreds of billions of dollars less than what they expect to need to pay for those benefits, even after 2021 returns hit a 30-year-record.

Pledging pension plan assets as collateral to borrow money to invest in alternative assets after a year that has seen the prices of most every asset class reach record highs, what could go wrong?

While my crystal ball doesn’t work any better than anyone else’s does, you don’t need to be an investment guru to see that this decision is desperation on the part of this pension to get the returns the pension needs to meet retirement payment obligations to the pension plan’s participants.

As long as the investments in which the pension plan invests the borrowed money continue to rise to new highs, the pension management board’s decision will make them look brilliant.

A more likely outcome in my view would be that at some point in the near future, the investments in which the borrowed money is invested will lose value and the pension will be in worse shape than it is now.

That’s when the fund looks to the government and begins to beg for bailouts.

Trouble is, also at some point in the fairly near future, the government will be forced to rein in spending or risk the integrity of the currency. As Alasdair Macleod noted in his recent piece titled “Returning to Sound Money” (Source: https://www.goldmoney.com/research/goldmoney-insights/returning-to-sound-money):

The growth in the M1 quantity since February 2020 has been without precedent exploding from $4 trillion, already a historically high level, to nearly $20 trillion this September. That is an average annualized M1 inflation of 230%. It is simply currency debasement and has yet to impact prices fully. Much of the increase has gone into the financial sector through quantitative easing, so its progress into the non-financial economy and the effects on consumer prices are delayed — but only delayed — as it will increasingly undermine the dollar’s purchasing power.

Those are remarkable numbers when you pause and consider them. The M1 money supply has expanded by 230% per year since February of 2020. Given that economists are in near universal agreement that the time lag between currency creation and the subsequent inflation is 18 months to 24 months, we haven’t begun to see the full effects of this currency creation.

The inflation that we are now experiencing is, in my view, a preview of coming events.

This will create a problem for pension plan investments as well as an additional problem. Pensions that have borrowed money to invest will likely see those investments perform negatively because of inflation and those pension participants who ultimately get a monthly income from the pension will see that pension buy a lot less.

This week’s radio program is an interview with Dr. A. Gary Shilling, long-time “Forbes” columnist, and “Bloomberg” contributor. He is also the publisher of the “Insight” newsletter.

I get Dr. Shilling’s market forecast and his view of the current health of the US economy. We also discuss the labor market and what that will look like next year in detail. Listen to the show now by clicking on the "Podcast" tab at the top of this page.

“If a man empties his purse into his head, no one can take it away from him. An investment in knowledge always pays the best interest.”

-Benjamin Franklin