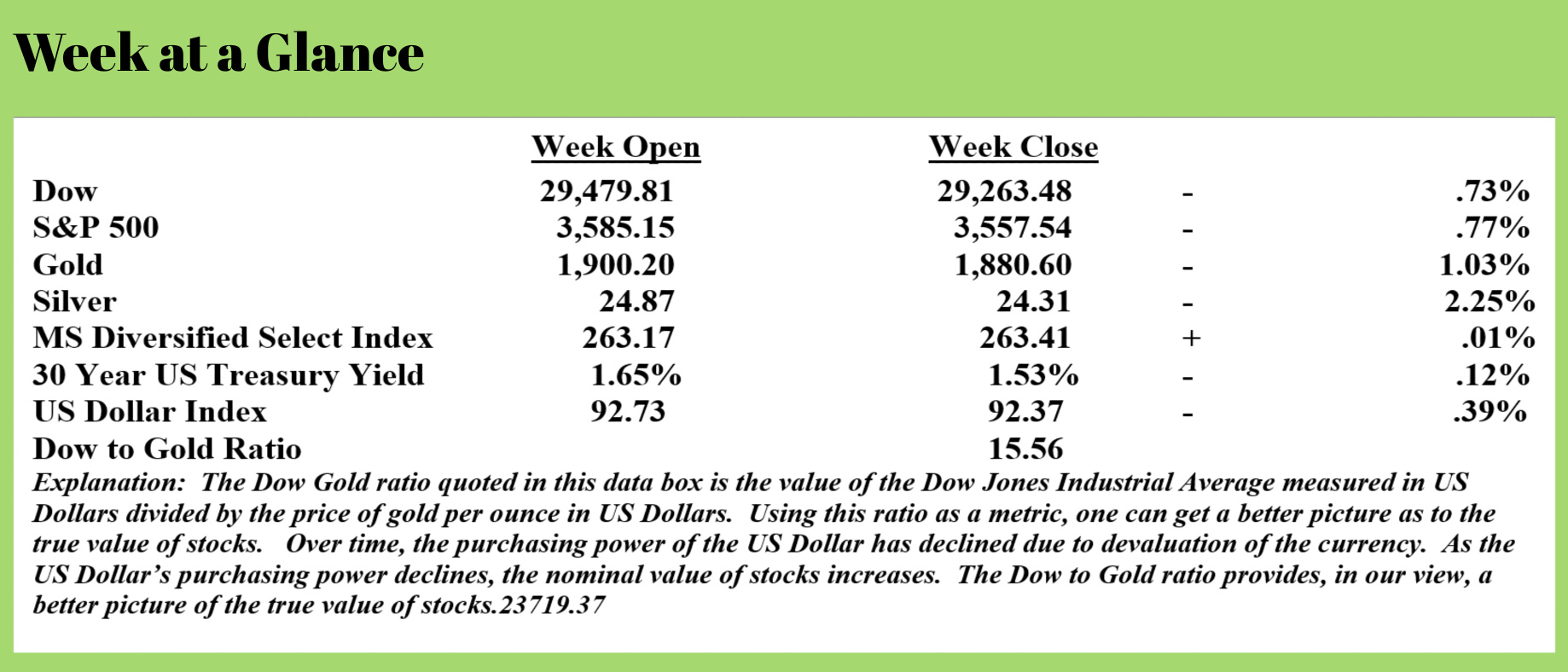

Weekly Market Update by Retirement Lifestyle Advocates

Weekly Market Update by Retirement Lifestyle Advocates

In the November client newsletter “The You May Not Know Report”, we wrote about a proposed “Great Reset”. The World Economic Forum, a group of world elites, meets each year in Davos, Switzerland to discuss and purportedly solve the problems facing the world. The Great Reset is an openly stated goal of this group. (Reference: https://www.weforum.org/agenda/2020/06/now-is-the-time-for-a-great-reset/)

We would encourage you to read about the goals of this group on your own and do your own research. For purposes of today’s discussion, here are some excerpts from the World Economic Forum’s website regarding the desired goals of the “Great Reset”:

The Great Reset agenda would have three main components. The first would steer the market toward fairer outcomes.

Moreover, governments should implement long-overdue reforms that promote more equitable outcomes.

The second component of a Great Reset agenda would ensure that investments advance shared goals, such as equality and sustainability. this means, for example, building “green” urban infrastructure and creating incentives for industries to improve their track record on environmental, social, and governance (ESG) metrics.

The third and final priority of a Great Reset agenda is to harness the innovations of the Fourth Industrial Revolution to support the public good, especially by addressing health and social challenges. During the COVID-19 crisis, companies, universities, and others have joined forces to develop diagnostics, therapeutics, and possible vaccines; establish testing centers; create mechanisms for tracing infections, and deliver telemedicine. Imagine what could be possible if similar concerted efforts were made in every sector.

Admittedly, we view the world through the lens of liberty and honest capitalism. We also readily acknowledge that there are problems with the system of capitalism in which we now find ourselves; namely, a playing field that is not level due to special government favors offered to certain businesses and specific industries. However, the socialistic goals of the World Economic Forum which can only be achieved through additional massive spending programs funded by freshly created currencies won’t solve any problems; instead, it will enrich the elite who may end up paying nominally higher taxes while the working class suffers.

That is what the current Federal Reserve system does. Pursuing the goals of “The Great Reset” as described by the WEF would only further exacerbate the wealth gap.

Past radio show guest, John Mauldin, in his newsletter “Thoughts from the Frontline” commented on this proposed “Great Reset” by the WEF. Here is an excerpt from his letter this past weekend (emphasis added) (Source: https://www.mauldineconomics.com/frontlinethoughts/the-great-reset-vs.-the-great-reset):

WEF calls this effort its “Great Reset Initiative.” For the record, it has nothing to do with my conception of The Great Reset. In fact, I think much of what they propose will make the version that I see even worse. I agree capitalism has gone off track and needs some adjustments, and not just minor ones. The current morass of crony capitalism and lobbying for special government favors is abhorrent. But “revamp all aspects of our societies and economies” sounds ominous. Especially coming from the people already nominally running the global economy.

Furthermore, what they really propose is that we change our lives while Davos Man continues undisturbed, maybe paying a few more taxes but with the brunt of the change affecting those further down the food chain. And, of course, they are not long on specifics.

When you start talking about resetting the educational and social contracts and working conditions, you are talking a radical social agenda. I believe we are going to have to have considerable change in the social structure of this country. That is what the current partisan politics is telling us. Too many people on both sides feel the current “social contract,” whatever you might think it is, is not working for them. Income and wealth inequality are very real. I am not convinced a WEF-style “Great Reset” is the answer.

One of the world elites calling for a reset of capitalism is Canadian Prime Minister, Justin Trudeau who recently said this about the reset (Source: https://torontosun.com/opinion/editorials/editorial-trudeau-sees-pandemic-as-an-opportunity) (emphasis added):

If it wasn’t coming from the horse’s mouth, nobody would believe it.

Prime Minister Justin Trudeau thinks the pandemic is an “opportunity” to enact a reset upon the Canadian economy, one that’s in line with a United Nations project called Agenda 2030 and consistent with his climate change goals.

It sounds like the stuff of conspiracy theories. It sounds like it can’t be true.

But it is.

“Building back better means getting support to the most vulnerable while maintaining our momentum on reaching the 2030 agenda for sustainable development,” says Trudeau. “This is our chance to help your pre-pandemic efforts to reimagine economic systems that actually address global challenges like extreme poverty, inequality, and climate change.”

While we would again encourage you to do your own research on Agenda 2030, here are some excerpts from the United Nation’s document describing the initiative (Source: https://thenewamerican.com/un-agenda-2030-a-recipe-for-global-socialism/):

(Agenda 2030) calls on the UN, national governments, and every person on Earth to “reduce inequality within and among countries.” To do that, the agreement continues, will “only be possible if wealth is shared and income inequality is addressed.”

By 2030, ensure that all men and women, in particular the poor and the vulnerable, have equal rights to economic resources.

“We commit to making fundamental changes in the way that our societies produce and consume goods and services,” the document states. It also says that “governments, international organizations, the business sector and other non-state actors and individuals must contribute to changing unsustainable consumption and production patterns … to move towards more sustainable patterns of consumption and production.”

In plain English, this could mean global wealth taxes and more government control, if not outright ownership of the means of production. History teaches us this never ends well. For example, ask the people of Venezuela how they fared once the country’s oil industry was nationalized.

While the objectives of eliminating poverty and closing the wealth gap sound noble enough, higher taxes and socialism just make the problems that much worse.

Past radio program guest and former Presidential candidate, Ron Paul had this to say on this subject (Source: https://www.silverdoctors.com/headlines/world-news/class-warfare-fed-counterfeiting-lockdowns-hammer-the-poor-and-middle-class/) (emphasis added):

The Fed’s counterfeiting of dollars hits the poor and those on fixed incomes like a sledgehammer. Inflation leads to there never being enough money at the end of the month. To make matters worse, unnecessary COVID lockdowns have slammed middle-class small businesses, while crony politically-connected corporations made out like bandits. Free markets and sound money are desperately needed to return to an economic reality that has been lost on America since the Fed was founded in 1913.

Indeed, when reviewing a list of attendees of the WEF 2019 meeting in Davos, one finds most attending are world government and business leaders. Small, independent business owners are not represented.

While a reset is inevitable, and a planned reset would be preferred, the “Great Reset” proposed by the WEF will only widen the wealth gap and lead to more money printing. This will lead to another reset.

Dr. Paul’s comment about a return to real free markets and sound money would be essential components in a planned reset in our view.

As we have noted in the past, current financial and economic trends are unsustainable. Lockdowns make matters worse. Absent a planned reset with sound money, current trends will only intensify and inflation or hyperinflation will be the inevitable result.

To that end, we have been developing strategies that can be used in the ‘two-bucket’ approach to managing money. The second bucket in the two-bucket strategy is designed to contain assets that will perform well in an inflationary environment. While we will be contacting clients about these additional strategies after the first of the New Year, once the dust settles on politics and possible policy changes, we will, in the meantime, offer some of our perspectives and observations relating to these strategies.

For many investors, we believe it makes sense to add to silver holdings at this juncture, particularly on more speculative assets. We conclude this for two reasons. One, Standard Charter Bank, an Indian Bank, has begun to aggressively purchase 1000 oz bars of silver competing with JP Morgan. Standard Charter is paying an exceptionally large premium to spot to acquire significant amounts of silver. (Source: https://www.silverdoctors.com/silver/silver-news/jp-morgan-faces-new-competition-in-the-physical-silver-market/) Two, increasingly, precious metals investors are standing for delivery on their metals which creates additional demand for physical metals.

As we develop, monitor, and research strategies on both strategic and tactical investments, we like holding some silver as a tactical investment.

This week’s radio program features an interview Alasdair Macleod. We chat with Alasdair about his view of looming inflation, and his view of the likelihood of a hyperinflationary outcome.

The interview is now available on the podcast which you can access through the RLA app.

If you don’t yet have the RLA app, you can download it by visiting www.RetirementLifestyleAdvocates.com.

The RLA app gives you free access to all our resources.

“Never be afraid to try something new. Remember, it was a lone amateur who built the ark. A team of professionals built the Titanic.”

-Dave Barry