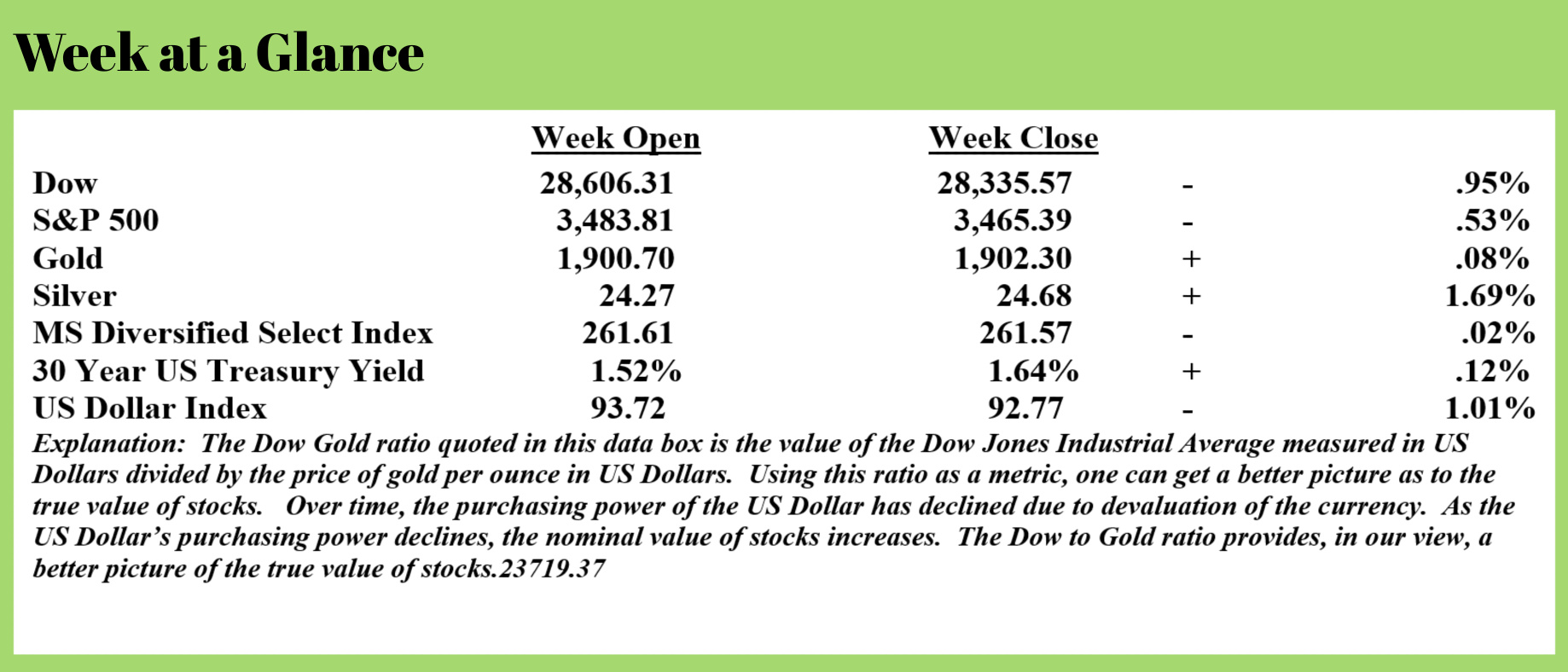

Weekly Market Update by Retirement Lifestyle Advocates

Weekly Market Update by Retirement Lifestyle Advocates

In this week’s “Portfolio Watch”, we’ll dig into some major and rather rapidly developing stories relating to currencies.

These stories have gone largely unnoticed given all the other news stories circulating; however, there are still some true journalists that exist and report on stories that could have a major effect on the lives of everyday Americans.

These developments are evolving quickly and should be on the radar of everyone, given that currency is perhaps the second or third most important commodity in our lives perhaps right behind oxygen and perhaps food.

As we have reported, there is growing evidence that central banks around the world are moving in the direction of digital currencies. While the idea of a digital currency is nothing new given that Bitcoin has existed for a decade or so, the migration of central bankers to digital currencies is relatively new,

By way of background, we should discuss the Money-Currency cycle. It’s a cycle that was identified in the 2015 best-selling book, “New Retirement Rules”. To be brief, with only slight variations, throughout history money has changed. It begins with money having tangible value, typically this stage of the money cycle has money being gold and/or silver. During this first stage of the Money-Currency cycle, money has intrinsic value; the money passed back and forth in commerce has real value.

The second stage of the Money-Currency Cycle sees money evolve from something tangible to a paper receipt that can be used to claim the tangible money. Most recently in US history, this would have been a paper silver certificate which was used until the 1960’s to claim ownership of coins that actually contained silver.

To briefly digress, if someone had a $10 silver certificate in the 1960’s and $10 in actual silver coins, the actual purchasing power of the paper and the silver was identical. If someone had the same $10 silver certificate today and the same $10 in silver coins, the purchasing power of each would be vastly different. The $10 silver certificate would have $10 in purchasing power but the $10 in silver coins contain 7.2 ounces of silver which would currently have the purchasing power of about $175.

The third stage of the Money-Currency Cycle has the currency used in commerce becoming a fiat currency. A fiat currency, by definition, is legal tender by fiat or government decree. The currency has little intrinsic, tangible value.

This has been the US Dollar since 1971. It also now describes every currency in the world. Think about this. A $100 bill has the same intrinsic value as a $1 bill; tangibly speaking they have the same value. The reason that a $100 bill has 100 times the purchasing power of the $1 bill is the printing on the bill. By contrast, using silver currency from the 1960’s as an example, it took 100 times more silver to have 100 times more purchasing power. The logic of that system is irrefutable. There is no logic when it comes to fiat currencies.

The final stage of the Money-Currency Cycle sees the fiat currency fail. This happens due to excessive money creation almost always to ‘paper over’ government deficit spending. This is the case presently. As Alasdair Macleod pointed out in a recent article that was referenced in last week’s “Portfolio Watch”, when the US Government’s operating deficit is calculated from March of this year on an annualized basis, the operating deficit is approximately $4.4 trillion, a number that dwarfs tax receipts.

While the final stage of the Money-Currency Cycle is not yet here, based on these numbers, it can’t be far away. At the present time, the Federal Reserve, the central bank of the United States is simply ‘papering over’ the mammoth operating deficit. Applying a little critical thinking to this current situation has one concluding that this cannot continue long-term.

Yet, as we write this 6 days before it is published, there is another stimulus package being considered, perhaps more than $2 trillion. Politicians are making promises of free stuff and monster new spending programs that would make $2 trillion look like pocket change are being proposed. Without commenting on the merits of any proposed program, the math is brutally clear, such programs cannot be funded by increased taxes, there is simply not enough money in existence to do so. Forget the billionaire tax rhetoric, confiscating 100% of the wealth of billionaires would raise about $8 trillion and cover the current year’s operating deficit with a mere trillion or so leftover depending on the size of the next stimulus package and perhaps the one after that.

These numbers make it obvious that we are nearing the end of the Money-Currency Cycle. As we have often written, it is far easier to forecast the ‘what’ than it is to forecast the ‘when’.

In this case, the ‘what’ is inevitable; we are only debating the when.

As we noted at the beginning of this piece, there is a lot of discussion taking place as far as currency changes are concerned. These discussions were whispers not long ago, now they are published stories.

In past issues, we have reported that many countries around the world were testing digital currencies, or to be more accurate, central bank digital currencies. Ukraine, Uruguay, the Bahamas, and parts of China are a few countries that are testing CBDC’s.

Now the Federal Reserve is openly discussing central bank-issued digital currencies.

From Reuters (Source: https://www.reuters.com/article/us-usa-fed-brainard/fedcoin-the-us-central-bank-is-looking-into-it-idUSKBN1ZZ2XF):

The Federal Reserve is looking at a broad range of issues around digital payments and currencies, including policy, design and legal considerations around potentially issuing its own digital currency, Governor Lael Brainard said on Wednesday.

Such a digital currency might be called “FedCoin” according to a NASDAQ article (Source: https://www.nasdaq.com/articles/fedcoin-could-replace-dollar-we-know-it-2017-04-14)

“The Economic Policy Journal” commented on this potential development (Source: https://www.economicpolicyjournal.com/2020/02/federal-reserve-board-governor-fed-is.html) (Brainard referenced in this excerpt refers to Federal Reserve Governor Lael Brainard)

“By transforming payments, digitalization has the potential to deliver greater value and convenience at a lower cost,” Brainard said.

“Some of the new players are outside the financial system’s regulatory guardrails, and their new currencies could pose challenges in areas such as illicit finance, privacy, financial stability, and monetary policy transmission,” she said.

But she added that the Fed is also “conducting research and experimentation related to distributed ledger technologies and their potential use case for digital currencies, including the potential for a CBDC (central bank digital currency).”

“We are collaborating with other central banks as we advance our understanding of central bank digital currencies,” she said.

It appears they are beginning to consider how to shutdown private cryptocurrencies and introduce their own.

We have reported in the past that the European Central Bank trademarked the term Digital Euro and the Bank of Japan has openly stated it was working on a digital currency as well.

A recent “Reuters” article confirmed that seven, world central banks are now collaborating on a digital currency (Source: https://www.reuters.com/article/bis-currency-digital-int-idUSKBN26U0KO)

Bank of England (BoE) Deputy Governor and chair of a BIS committee on payments Jon Cunliffe said the rise in cashless payments since lockdowns to fight the pandemic has accelerated how technology is changing forms of money.

Central banks need to keep up to avoid the private sector plugging payments gaps in unsuitable ways, Cunliffe said.

Besides the Fed and the BoE, the seven central banks that have teamed up with the BIS include the European Central Bank, the Swiss National Bank, and Bank of Japan, but not the People’s Bank of China.

China is already piloting a digital renminbi, with the PBOC saying it would boost the yuan’s reach in a world currently dominated by the dollar.

At this point, from our research, it seems that all these digital currencies would be central bank-issued and not backed by tangible assets like gold or silver. The fact that these proposed digital currencies would continue to be fiat, doesn’t solve any of the issues facing fiat currencies presently. Without a CBDC backed by something tangible, the Money-Currency Cycle may be extended for a time but ultimately the fiat money problems will become even worse.

These CBDC’s, should they become reality in fiat form, do raise a couple of red flags.

The first issue is the issue of financial privacy. If a digital currency were to be used exclusively, every transaction would be tracked, and prohibiting certain transactions would be easy.

The second issue is that should a digital currency become exclusively used, it would be easy for banks to impose negative interest rates. While the whole concept of negative interest rates would have been laughable 10 years ago, they have now become reality in many parts of the world.

It is our view that a fiat digital currency would simply accelerate the inflation cycle. Faced with a choice of owning a tangible asset or paying negative interest rates to park a fiat digital currency in a bank, what choice would most consumers make?

What choice would you make?

This week’s radio program is a ‘best of’ program featuring an interview with prolific author, Jeffrey Tucker of the American Institute for Economic Research. We chat with Jeffrey about his recently released book “Liberty or Lockdown”.

The interview is now available on the podcast which you can access through the RLA app. If you don’t yet have the RLA app, you can download it by visiting www.RetirementLifestyleAdvocates.com.

The RLA app gives you free access to all our resources.

“I’ve had a perfectly wonderful evening. But this wasn’t it.”

-Groucho Marx