Weekly Update from RLA Tax and Wealth Advisory

Weekly Update from RLA Tax and Wealth Advisory

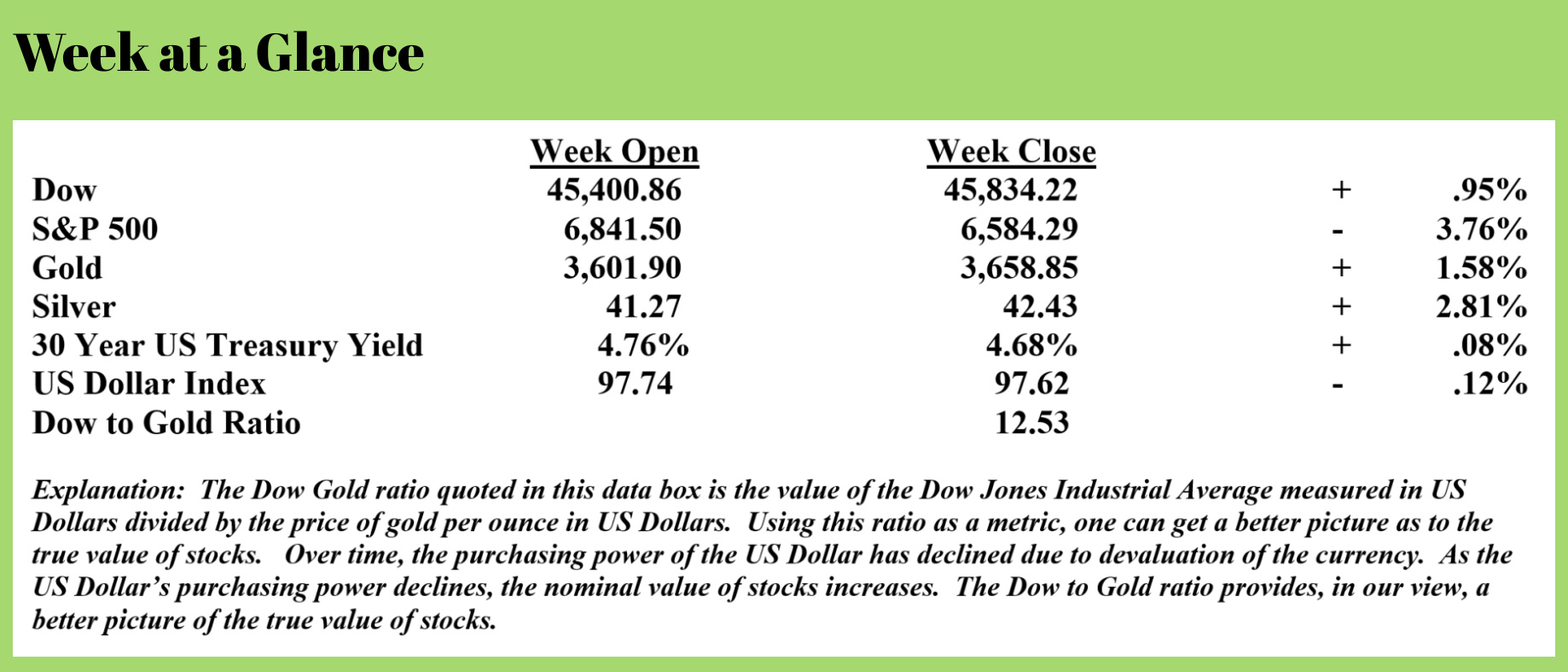

By: Dennis Tubbergen

More Proof a Debt Crisis Is Inevitable

Notice that I did not say a debt crisis is imminent – but it is inevitable. However, as I noted in this short newsletter last week, it may be getting close as interest rates that world governments are paying to finance and refinance debt are rising literally across the board.

Focusing on the United States, the trajectory of government debt accumulation is on a scale that is totally unsustainable. The “Kobeissi Letter” published a statistic last week that is nothing short of mind-boggling – by 2055, the United States’ government debt will reach $150 trillion, and that’s according to the estimate of the Congressional Budget Office. (Source: https://marketsanity.com/the-us-debt-crisis-is-set-to-get-even-worse/)

That would push the national debt to gross domestic product ratio to 169% up from the current level of 123%! For perspective, over the past 50 years, the US Government debt-to-GDP ratio has averaged 69%.

According to Congressional Budget Office estimates, the federal government’s operating deficit will exceed 5% of GDP every year for the next 30 years. That begs the all-important question: how will the policymakers and politicians attempt to fund this monster shortfall?

Given that the problem is too large to solve via increased taxes and given that it seems there is zero political will on either side of the aisle to rein in spending, there is only one remaining option – create currency.

That is exactly what has happened historically, and mark my words, it is what will happen again. Have you taken appropriate steps in your portfolio to potentially profit from more easy money policies?

Inflation Is Still Here But the Fed Will Likely Cut Interest Rates Anyway

The most recent inflation data reflects a continuing inflation problem. Core services, which include essentials like housing, healthcare, and insurance, rose by 4.3% on an annualized basis from July to August. (Source: https://wolfstreet.com/2025/09/11/cpi-inflation-dishes-up-another-nasty-surprise-as-it-tends-to-do/). That’s the second month in a row that core services inflation rose by more than 4% on an annualized basis.

The largest price increases came from used vehicle prices. Food and gasoline prices also jumped.

Core CPI, which does not include food prices or energy costs, jumped .35% from July to August. That translates to an annualized rate of 4.2%. That is the worst level since January. When food and energy prices are included, the annualized inflation level is 4.7%.

These rising inflation numbers don’t suggest a Federal Reserve interest rate cut may be warranted, but I expect that we will see one anyway. Look for that to further fuel inflation, although, as we have often discussed in this publication, there will be a time lag between the policy change and the effects of the policy change.

A Banking Rule Change that May Hide How Much Trouble Some Banks May Be Having

Thanks to a client for sharing the article referenced here with me last week.

There is a change coming to the reporting rules that govern how banks report loans that have been modified to keep buyers from defaulting.

Beginning this fall, US banks will no longer have to disclose the total outstanding amount of loans whose terms have been modified to keep borrowers from falling behind. Up to this point, a loan whose terms had been modified needed to be flagged as such for the life of the loan. This reporting standard has been in place since the 1970s, or about 50 years.

Under the new reporting rules, banks only need to report the loans that have had their terms modified within the prior 12 months. (Source: https://www.saferbankingresearch.com/article/Banks-Are-Hiding-How-Much-Trouble-They-Are-In-202509031926.html)

Obviously, this reporting change will make it more difficult to determine the health of a bank’s loan portfolio.

Not surprisingly, the leading advocate for the reporting changes was The Bank Policy Institute, a lobbying group representing JP Morgan, Citigroup, and Goldman Sachs.

Savvy readers will be asking why big banks were strongly advocating for these changes (The Bank Policy Institute orchestrated a big marketing campaign for these changes last year, according to the article referenced above.)

That question answers itself. Unless there have been excessive levels of loan modifications that banks want to hide, there would be no reason to push for these changes.

There is another reason to consider holding assets outside the banking system.

Is AI in a Bubble?

This past week at an event at which I spoke, I had a conversation with an audience member about artificial intelligence. This individual was convinced that AI stocks were going to keep rising as the technology continues to improve and evolve.

I respectfully dissented. While I believe that the emergence of AI technology is one of the biggest developments in a very long time, it also seems obvious that AI-related stocks are in a bubble that will have to burst at some future point.

The current AI bubble is reminiscent of the dot.com bubble of twenty-five years ago. As you older readers may recall, there were massive levels of hype surrounding nearly every dot.com stock that had a stock offering in the late 1990s. This drove the NASDAQ to record highs before it ultimately crashed by 80%. Incidentally, it took more than twenty years for the NASDAQ to recover.

The dot.com stock crash didn’t mean that the technology was invalidated; it just meant that investors became irrational. The current AI craze is just a dot.com rerun. The technology is here to stay and will be a part of our lives moving ahead, but that fact doesn’t mean AI investors are rational.

RLA Radio

The RLA radio program this week features an interview that I did with Mr. Peter Schiff, where he shares his views on dollar debasement, government overreach, and the coming financial crisis.

The program is available now by clicking on the "Podcast" tab at the top of this page.

Quote of the Week

“Clothes make the man. Naked people have little or no influence on society.” -Mark Twain

Comments