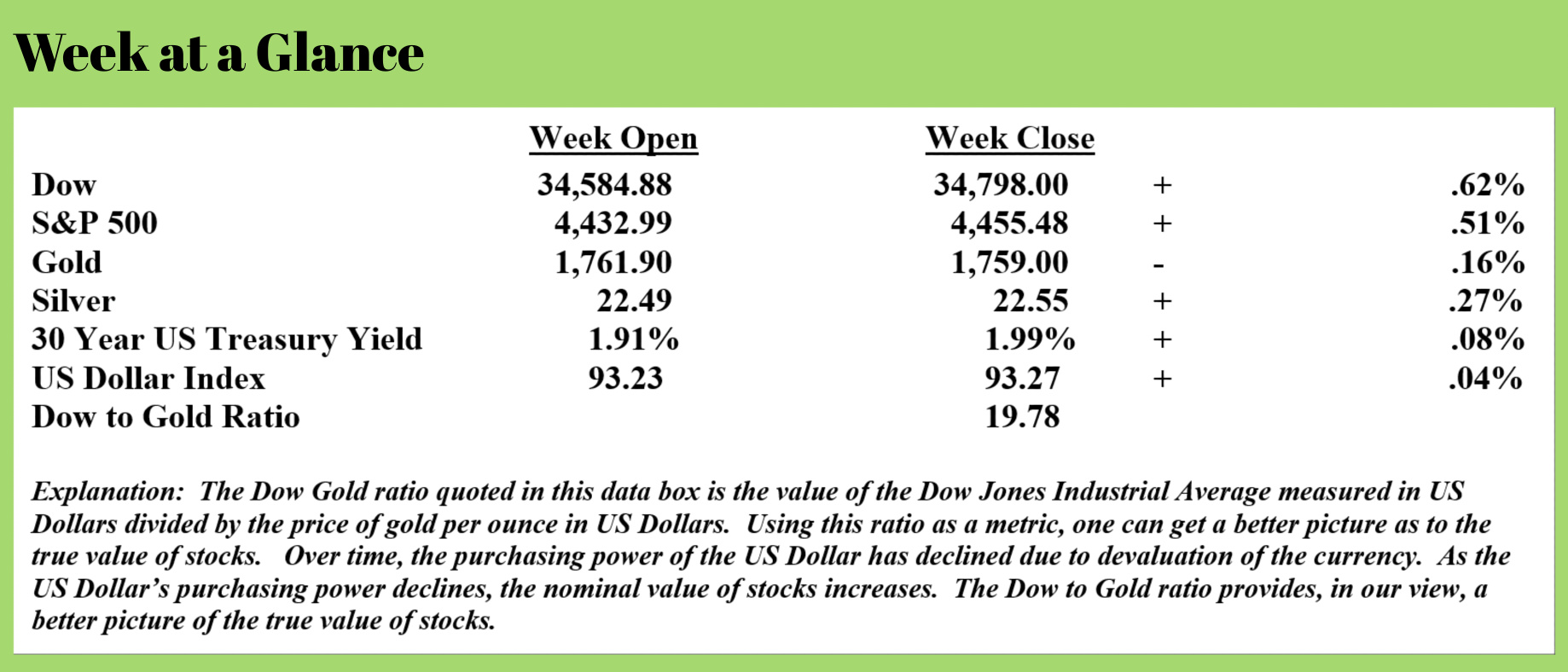

Weekly Market Update by Retirement Lifestyle Advocates

Weekly Market Update by Retirement Lifestyle Advocates

This week’s “Portfolio Watch” will be a bit different than what you are used to seeing each week. This week, I want to bring you up to speed on some proposed changes out of Washington relating to Roth IRA accounts.

I’ve often stated in this weekly publication and on my radio program and podcast that I am of the opinion that the tax-hungry politicians will find retirement accounts a difficult target to resist given the numbers

According to the Investment Company Institute, at the close of the first quarter of 2021, the total assets held in retirement accounts in the United States was $35.4 trillion. (Source: https://www.ici.org/statistical-report/ret_21_q1)

Given that the ‘official’ national debt is approaching $30 trillion, if politicians could get their hands on the retirement account assets, the nation’s fiscal problems could be solved temporarily. Actually very temporarily given the downright out-of-control spending that has been characteristic of Washington politicians for the past couple of decades. As we are all keenly aware, spending by the Washington politicians has only grown increasingly irresponsible and wild as time has passed.

But, I digress.

In my book “Economic Consequences”, published ten years ago, I first made this point. At that time, the Fed had recently begun quantitative easing or currency creation out of thin air as a temporary, emergency measure.

I suggested in the book that history taught us currency creation programs were rarely temporary, rather they become policy until the consequences of currency creation are worse than dealing with the consequences of debt excesses. I also suggested that retirement accounts would likely prove to be a tantalizing tax target.

In the book, I offered examples of countries that had actually taken control of some of the retirement accounts of the citizens by requiring that retirement account assets be invested in that country’s government bonds “in the interest of retirement safety and stability.”

I also suggested that politicians could raise significant revenues at the expense of those who’s worked hard and accumulated assets in retirement accounts by changing tax laws.

Fortunately, there has been no requirement to invest retirement account assets in government bonds, but over the past year or so, tax rules relating to IRA’s and other retirement accounts have changed.

For example, the SECURE Act, while raising the age at which required minimum distributions need to be taken from a retirement account from 70 ½ years old to age 72, also killed the stretch out IRA.

If you’re not familiar with a stretch-out IRA, it allowed a non-spouse beneficiary on a retirement account (typically a child), to inherit an IRA and spread the unpaid tax liability out over the beneficiary’s lifetime. For example, a 50-year old inheriting an IRA with a 35-year life expectancy could use a stretch-out IRA by taking a distribution of 1/35th of the inherited IRA account in year one; followed by a distribution the next year of 1/34th of the remaining account and so on.

After the SECURE Act, all taxes on an inherited IRA must generally be paid within 10 years.

In my latest book, “Retirement Roadmap”, I do a hypothetical analysis on how this affects the beneficiary of a retirement account. I assume a 50-year old inherits a $1,000,000 IRA before the SECURE Act became law and used the stretch-out option. Assuming the inherited IRA account grows at a rate of 5% per year and the 50-year old beneficiary is in the 25% tax bracket, the beneficiary realizes an after-tax net of more than $1.9 million from the $1 million inherited IRA.

If we use the same 5% growth assumption for inherited IRA assets but now assume the taxes on the inherited IRA need to be paid within 10 years, the IRA beneficiary now receives an after-tax net of about half of what the beneficiary would have received using the stretch out strategy.

Even more interesting is the IRS’ tax take over the first 10 years after inheritance. After the SECURE Act, based on our stated assumptions, the IRS receives more than $225,000 in additional taxes during the first 10 years!

It’s no wonder that when the SECURE Act was proposed, “The Wall Street Journal” ran an op-ed piece titled “They’re Coming for Your IRA”.

Now, the Washington politicians are at it again; proposing more IRA tax changes as well as limits on Roth conversions. Here are selected excerpts from a recent article in “The Wall Street Journal” (Source: https://www.wsj.com/articles/retirement-savers-love-the-backdoor-roth-ira-strategy-it-might-not-last-11632475801?mod=e2fb&fbclid=IwAR0J8fibwyR5_YDYP7UIPm--rJ47yrItWmzPpgixmR_VxPJb8uC-iD8CgCo)

Many Americans are using a previously little-known tax method to boost their savings. Now, the government is trying to stop it.

The tax strategy at issue is the mega-backdoor Roth conversion and it has allowed some Americans to amass sizable balances in tax-free Roth retirement accounts. On Sept. 15, the House Ways and Means Committee approved legislation from House Democrats that would prohibit the use of the mega-backdoor Roth conversion starting Jan. 1, 2022.

The proposal is one of a series of measures Democrats are backing in an effort to prevent the wealthiest Americans from shielding multimillion-dollar retirement balances from taxes. The move is part of a broader agenda that includes raising taxes on higher-income Americans and cracking down on tax avoidance to help pay for measures including the party’s $3.5 trillion healthcare, education, and climate bill.

The legislation also proposes eliminating Roth conversions of after-tax contributions to traditional individual retirement accounts starting Jan. 1, 2022. It would require most people with aggregate retirement-account balances above $10 million to take distributions, regardless of their age. And it would ban holding unregistered securities, including private equity, in IRAs.

Starting in 2032, the legislation would prevent single people earning more than $400,000 a year and married couples with incomes above $450,000 from converting pretax retirement-account money to Roth accounts.

Admittedly, the proposed changes won’t affect the majority of those who do Roth IRA conversions or participate in company retirement plans, at least initially.

Color me cynical, but being a student of history and studying how taxes and tax policy come to be, tax changes and tax increases are always imposed on the high earners first. But then, more times than not in my judgment, these tax increases, and tax changes extend to more and more taxpayers.

For example, when the income tax was introduced in 1913, it originally significantly affected only VERY high earners.

After a $3,000 standard deduction, the income tax rate was 1% to $20,000. Only income earners who had incomes in excess of $500,000 were taxed at a rate of 7%.

Let me attempt to put those numbers in context, adjusting for the diminished purchasing power of today’s US Dollar.

Today’s dollar has lost more than 96% of its purchasing power since 1913. That means a dollar today is the 1913 equivalent of 4 cents.

Doing a little math, one quickly concludes that a $3,000 standard deduction in 1913 would be the equivalent of a $75,000 deduction today.

Imagine getting a $75,000 deduction and then paying income tax of 1% on income over and above the $75,000 until your income reached the 1913 equivalent of $20,000 or about $500,000 today.

The top tax bracket in 1913, 7% on incomes over $500,000 would be like entering the highest tax bracket today with $12,500,000 of income.

In 1913, there was no tax withholding by employers. However, after-tax withholding began and the Social Security Act was passed, even part-time employees were paying taxes.

My point is this – if you have not seriously examined a Roth conversion strategy for your individual financial situation, you should do so.

I discuss this at length in my recent book “Retirement Roadmap” which was a number one Amazon best-seller thanks to many of you supporting the book.

Given the negative tax momentum surrounding retirement accounts presently and the fact that tax rates will increase in 2026 if Congress doesn’t change them before that, now may be the perfect time to look at the ultimate tax liability on your retirement accounts.

Procrastinating could be costly.

This week’s radio program features an interview with the David Mcalvany of Mcalvany Financial.

David is a very bright market and economic analyst. I get his forecast for the economy and financial markets moving ahead.

Don’t miss the interview. Click on the "Podcast" tab at the top of this page to listen to the show.

“Opportunity is missed by most people because it is dressed in overalls and looks like work.”

-Thomas Edison